Page 14: of Offshore Engineer Magazine (Sep/Oct 2023)

Read this page in Pdf, Flash or Html5 edition of Sep/Oct 2023 Offshore Engineer Magazine

13

13

15

15

MARKETS OFFSHORE SUPPORT VESSELS

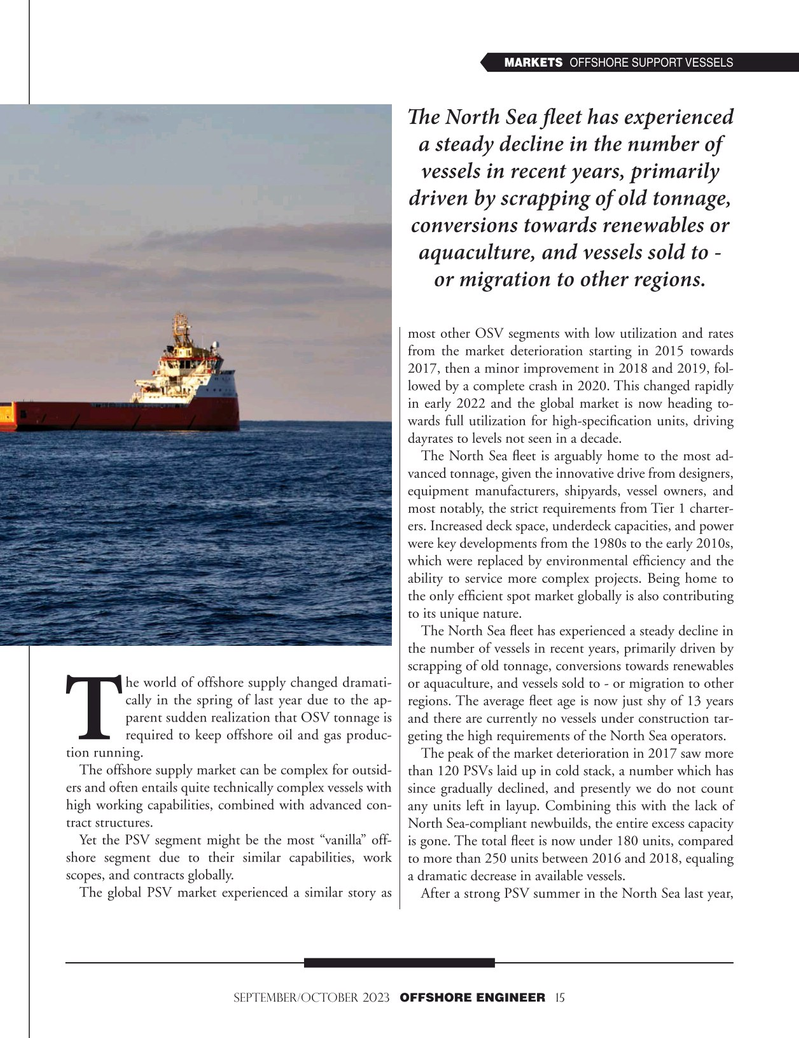

Te North Sea feet has experienced a steady decline in the number of vessels in recent years, primarily driven by scrapping of old tonnage, conversions towards renewables or aquaculture, and vessels sold to - or migration to other regions. most other OSV segments with low utilization and rates from the market deterioration starting in 2015 towards 2017, then a minor improvement in 2018 and 2019, fol- lowed by a complete crash in 2020. This changed rapidly in early 2022 and the global market is now heading to- wards full utilization for high-speci?cation units, driving dayrates to levels not seen in a decade.

The North Sea ?eet is arguably home to the most ad- vanced tonnage, given the innovative drive from designers, equipment manufacturers, shipyards, vessel owners, and most notably, the strict requirements from Tier 1 charter- ers. Increased deck space, underdeck capacities, and power were key developments from the 1980s to the early 2010s, which were replaced by environmental ef?ciency and the ability to service more complex projects. Being home to the only ef?cient spot market globally is also contributing to its unique nature.

The North Sea ?eet has experienced a steady decline in the number of vessels in recent years, primarily driven by scrapping of old tonnage, conversions towards renewables he world of offshore supply changed dramati- or aquaculture, and vessels sold to - or migration to other cally in the spring of last year due to the ap- regions. The average ?eet age is now just shy of 13 years parent sudden realization that OSV tonnage is and there are currently no vessels under construction tar- required to keep offshore oil and gas produc- geting the high requirements of the North Sea operators.

T tion running. The peak of the market deterioration in 2017 saw more

The offshore supply market can be complex for outsid- than 120 PSVs laid up in cold stack, a number which has ers and often entails quite technically complex vessels with since gradually declined, and presently we do not count high working capabilities, combined with advanced con- any units left in layup. Combining this with the lack of tract structures. North Sea-compliant newbuilds, the entire excess capacity

Yet the PSV segment might be the most “vanilla” off- is gone. The total ?eet is now under 180 units, compared shore segment due to their similar capabilities, work to more than 250 units between 2016 and 2018, equaling scopes, and contracts globally. a dramatic decrease in available vessels.

The global PSV market experienced a similar story as After a strong PSV summer in the North Sea last year, september/october 2023 OFFSHORE ENGINEER 15