Page 13: of Offshore Engineer Magazine (Nov/Dec 2023)

Read this page in Pdf, Flash or Html5 edition of Nov/Dec 2023 Offshore Engineer Magazine

12

12

14

14

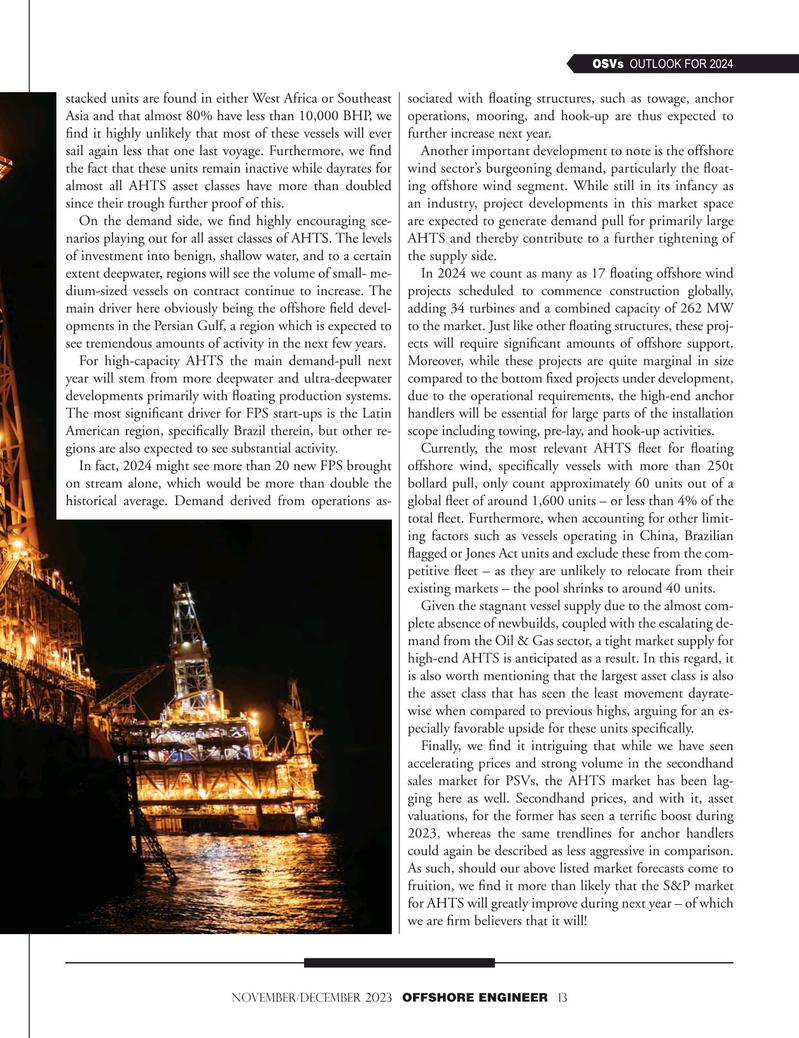

OSVs OUTLOOK FOR 2024 stacked units are found in either West Africa or Southeast sociated with foating structures, such as towage, anchor

Asia and that almost 80% have less than 10,000 BHP, we operations, mooring, and hook-up are thus expected to fnd it highly unlikely that most of these vessels will ever further increase next year. sail again less that one last voyage. Furthermore, we fnd Another important development to note is the offshore the fact that these units remain inactive while dayrates for wind sector’s burgeoning demand, particularly the foat- almost all AHTS asset classes have more than doubled ing offshore wind segment. While still in its infancy as since their trough further proof of this. an industry, project developments in this market space

On the demand side, we fnd highly encouraging sce- are expected to generate demand pull for primarily large narios playing out for all asset classes of AHTS. The levels AHTS and thereby contribute to a further tightening of of investment into benign, shallow water, and to a certain the supply side. extent deepwater, regions will see the volume of small- me- In 2024 we count as many as 17 foating offshore wind dium-sized vessels on contract continue to increase. The projects scheduled to commence construction globally, main driver here obviously being the offshore feld devel- adding 34 turbines and a combined capacity of 262 MW opments in the Persian Gulf, a region which is expected to to the market. Just like other foating structures, these proj- see tremendous amounts of activity in the next few years. ects will require signifcant amounts of offshore support.

For high-capacity AHTS the main demand-pull next Moreover, while these projects are quite marginal in size year will stem from more deepwater and ultra-deepwater compared to the bottom fxed projects under development, developments primarily with foating production systems. due to the operational requirements, the high-end anchor

The most signifcant driver for FPS start-ups is the Latin handlers will be essential for large parts of the installation

American region, specifcally Brazil therein, but other re- scope including towing, pre-lay, and hook-up activities. gions are also expected to see substantial activity. Currently, the most relevant AHTS feet for foating

In fact, 2024 might see more than 20 new FPS brought offshore wind, specifcally vessels with more than 250t on stream alone, which would be more than double the bollard pull, only count approximately 60 units out of a historical average. Demand derived from operations as- global feet of around 1,600 units – or less than 4% of the total feet. Furthermore, when accounting for other limit- ing factors such as vessels operating in China, Brazilian fagged or Jones Act units and exclude these from the com- petitive feet – as they are unlikely to relocate from their existing markets – the pool shrinks to around 40 units.

Given the stagnant vessel supply due to the almost com- plete absence of newbuilds, coupled with the escalating de- mand from the Oil & Gas sector, a tight market supply for high-end AHTS is anticipated as a result. In this regard, it is also worth mentioning that the largest asset class is also the asset class that has seen the least movement dayrate- wise when compared to previous highs, arguing for an es- pecially favorable upside for these units specifcally.

Finally, we fnd it intriguing that while we have seen accelerating prices and strong volume in the secondhand sales market for PSVs, the AHTS market has been lag- ging here as well. Secondhand prices, and with it, asset valuations, for the former has seen a terrifc boost during 2023, whereas the same trendlines for anchor handlers could again be described as less aggressive in comparison.

As such, should our above listed market forecasts come to fruition, we fnd it more than likely that the S&P market for AHTS will greatly improve during next year – of which we are frm believers that it will!

november/december 2023 OFFSHORE ENGINEER 13