Page 24: of Maritime Reporter Magazine (April 2005)

The Offshore Industry Anual

Read this page in Pdf, Flash or Html5 edition of April 2005 Maritime Reporter Magazine

23

23

25

25

24 Maritime Reporter & Engineering News

T he World LNG & GTL Report, published by Douglas-

Westwood, forecasts strong growth in expenditure on new

LNG plants and terminals. In this arti- cle, the author presents some of the thinking behind the report.

The level of interest in the LNG busi- ness continues to grow. Recent years have seen the completion of some major high-profile LNG projects, particularly around the Atlantic Basin. While demand remains strong in the traditional

Asian markets, much attention is now being directed to the opportunities aris- ing from the new and potentially vast

Atlantic Basic LNG market. Meanwhile, the limits of domestic gas production in

North America and Western Europe are becoming clear and gas import demands are rising. LNG is increasingly a method of choice in satisfying growing gas demand in these regions, and following the success of the plants recently estab- lished in Nigeria and Trinidad &

Tobago, a wave of new projects has emerged that demonstrate a potential for serious market growth over the next five years.

The Development of the LNG Sector

Gas liquefaction technology has its roots in the 19th century, pioneered by individuals such as Michael Faraday and

Karl Von Linde. However, the world- wide LNG trade began in earnest in the 1960s when, following a number of test shipments across the Atlantic to prove the concept, the first commercial LNG trade began between Algeria and the

UK. Although the UK may have led the way in adopting LNG technology, the region in which the LNG business really took off was Asia. Japan, which had no gas production of its own, was very quick to adopt the new technology, and was soon followed by countries such as

South Korea and Taiwan. Meanwhile in

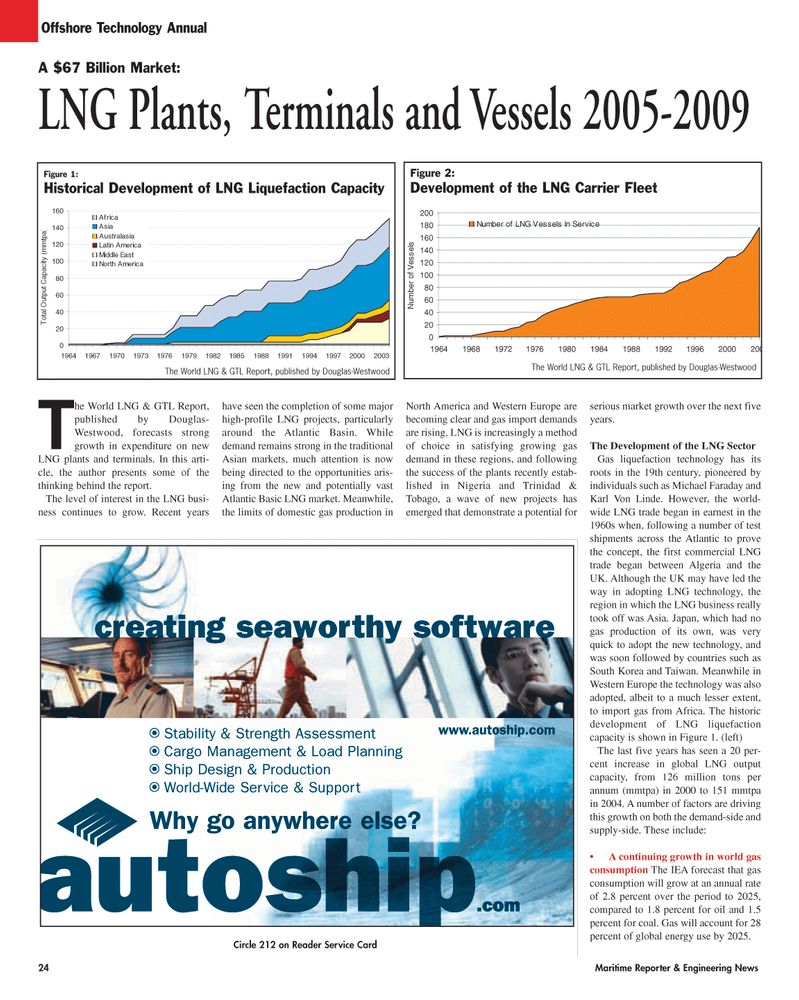

Western Europe the technology was also adopted, albeit to a much lesser extent, to import gas from Africa. The historic development of LNG liquefaction capacity is shown in Figure 1. (left)

The last five years has seen a 20 per- cent increase in global LNG output capacity, from 126 million tons per annum (mmtpa) in 2000 to 151 mmtpa in 2004. A number of factors are driving this growth on both the demand-side and supply-side. These include: • A continuing growth in world gas consumption The IEA forecast that gas consumption will grow at an annual rate of 2.8 percent over the period to 2025, compared to 1.8 percent for oil and 1.5 percent for coal. Gas will account for 28 percent of global energy use by 2025.

Offshore Technology Annual

Stability & Strength Assessment

Cargo Management & Load Planning

Ship Design & Production

World-Wide Service & Support creating seaworthy software www.autoship.com

Why go anywhere else?

Circle 212 on Reader Service Card 0 20 40 60 80 100 120 140 160 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003

T o t a l O u t put C a pac i t y ( mmt pa)

Africa

Asia

Australasia

Latin America

Middle East

North America

A $67 Billion Market:

LNG Plants, Terminals and Vessels 2005-2009

Figure 1:

Historical Development of LNG Liquefaction Capacity

The World LNG & GTL Report, published by Douglas-Westwood 0 20 40 60 80 100 120 140 160 180 200 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 200

N u m b e r o f V e sse l s

Number of LNG Vessels In Service

Figure 2:

Development of the LNG Carrier Fleet

The World LNG & GTL Report, published by Douglas-Westwood

MR APRIL 2005 #3 (17-24).qxd 4/1/2005 4:07 PM Page 8