Page 24: of Maritime Reporter Magazine (August 2010)

The Electric Ship

Read this page in Pdf, Flash or Html5 edition of August 2010 Maritime Reporter Magazine

23

23

25

25

24 Maritime Reporter & Engineering News

MARKET REPORT OFFSHORE FLOATING PRODUCTION SYSTEMS

Introduction & market overview

Over the next few years, Douglas-West- wood forecasts a strong increase in FPS expenditure, driven by a surge in instal- lations. Findings from the latest edition of our World Floating Production Market

Report indicate that more than 100 Float- ing Production Systems (FPSs) will be installed worldwide over the next five years. This represents a total global value of approximately $45 billion and around a 20% increase on the previous five years.

It is worth noting upfront that, follow- ing the Deepwater Horizon explosion and oil spill, President Obama has announced a ban on drilling in deepwaters (in depths greater 500 feet) by floating semi-sub- mersible drilling rigs and drillships cur- rently operating in the region. This will ultimately lead to a delay in the develop- ment of current and future offshore re- serves.

However, at this time we do not believe that the ban will affect any of the North

American FPS projects forecast to come onstream during the 2010-2014 period.

To date, Latin America has seen the greatest number of FPS installations and its forecast market share is equivalent to almost a third of global FPS Capex over the period. The region’s importance is al- most entirely due to the wave of deepwa- ter projects in the Santos and Campos

Basins off Brazil moving forward devel- opment in the next five years. Together,

Africa, Asia and Latin America account for almost two-thirds of the units forecast for installation over the next five years.

Asia is forecast for 23 installations, but only accounts for 12% of the expenditure as a number of the planned installations are redeployments which only require minimal Capex for upgrades. The rela- tively benign environments and shallow waters in which most of the FPS prospects in the region are located also allow cheaper FPS solutions to be adopted. In the Western Europe region, despite the fact that many of the produc- ing areas are now considered mature and significant new finds are becoming less frequent, there are still considerable de- velopment opportunities – with 18 planned installations.

Global FPS fleet

In terms of vessel type, FPSOs domi- nate the global floating production scene.

As of year-end 2009, there had been more than 220 FPSO deployments world- wide – almost double all the other float- ing production systems (semi-submersible FPSs, TLPs and

Spars) put together. There are currently more than 150 FPSOs in operation.

Africa and Asia have the largest fleets, followed by Latin America. It’s not sur- prising, therefore, that FPSOs represent by far the largest segment of the market, accounting for close to four-fifths of the total FPS forecast Capex. TLPs and semi- submersible FPSs form the next-largest segments around 10% of the market each (with Spars make up the remainder).

FPSSs have a long history and have proved particularly popular off Brazil where the national operator, Petrobras, has embraced FPS technology as a means of developing the country’s extensive deepwater reserves. There have been more than 80 FPSS installations world- wide; many of these were short-term de- ployments for early production or well testing purposes.

TLPs, and more recently Spars, have proved the production system of choice in the US Gulf of Mexico. More than half the TLP installations to date and all but one of the spars have been associated with deepwater developments in the US

Gulf. Recent years have seen the intro- duction of smaller, less expensive designs to enable the exploitation of marginal fields. However, the progression into ultra-deep waters in this region is now working in favour of FPSO solutions (with operators such as Petrobras bring- ing extensive FPSO experience) and against TLP designs, which are less fea- sible in ultra-deep waters.

Evaluating the

Floating Production Market 2010-2015

By Lucy Miller, Douglas-Westwood Ltd

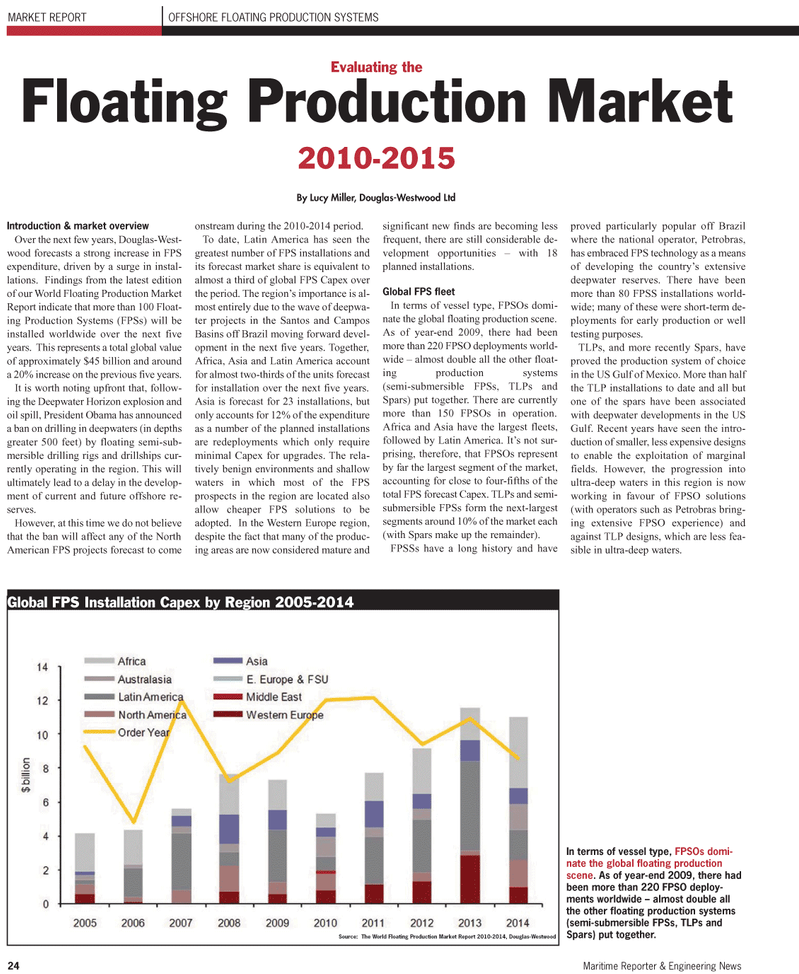

Global FPS Installation Capex by Region 2005-2014

Source: The World Floating Production Market Report 2010-2014, Douglas-Westwood

In terms of vessel type, FPSOs domi- nate the global floating production scene. As of year-end 2009, there had been more than 220 FPSO deploy- ments worldwide – almost double all the other floating production systems (semi-submersible FPSs, TLPs and

Spars) put together.