Page 64: of Maritime Reporter Magazine (September 2013)

Workboat Annual

Read this page in Pdf, Flash or Html5 edition of September 2013 Maritime Reporter Magazine

63

63

65

65

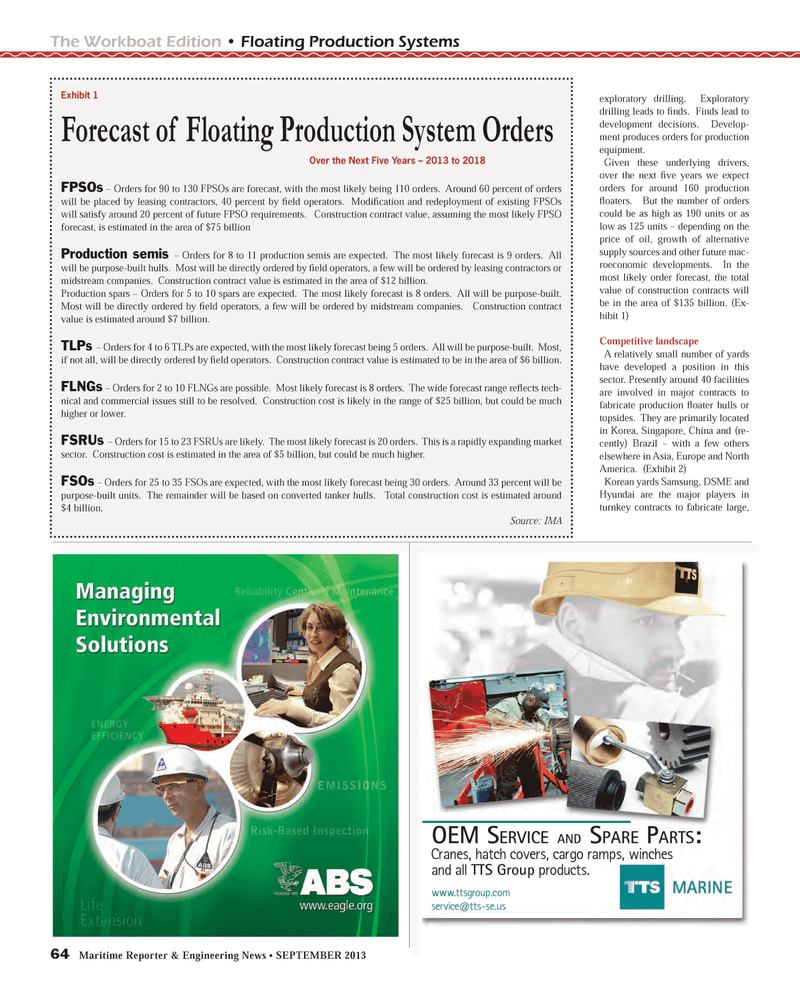

64 Maritime Reporter & Engineering News ? SEPTEMBER 2013 The Workboat Edition ? Floating Production Systemsexploratory drilling. Exploratory drilling leads to Þ nds. Finds lead to development decisions. Develop-ment produces orders for production equipment.Given these underlying drivers, over the next Þ ve years we expect orders for around 160 production ß oaters. But the number of orders could be as high as 190 units or as low as 125 units ? depending on the price of oil, growth of alternative supply sources and other future mac-roeconomic developments. In the most likely order forecast, the total value of construction contracts will be in the area of $135 billion. (Ex-hibit 1)Competitive landscapeA relatively small number of yards have developed a position in this sector. Presently around 40 facilities are involved in major contracts to fabricate production ß oater hulls or topsides. They are primarily located in Korea, Singapore, China and (re-cently) Brazil ? with a few others elsewhere in Asia, Europe and North America. (Exhibit 2)Korean yards Samsung, DSME and Hyundai are the major players in turnkey contracts to fabricate large, OEM SERVICE AND SPARE PARTS:Cranes, hatch covers, cargo ramps, winches and all TTS Group products. www.ttsgroup.com [email protected] 1Forecast of Floating Production System Orders Over the Next Five Years ? 2013 to 2018 FPSOs ? Orders for 90 to 130 FPSOs are forecast, with the most likely being 110 orders. Around 60 percent of orders will be placed by leasing contractors, 40 percent by Þ eld operators. Modi Þ cation and redeployment of existing FPSOs will satisfy around 20 percent of future FPSO requirements. Construction contract value, assuming the most likely FPSO forecast, is estimated in the area of $75 billionProduction semis ? Orders for 8 to 11 production semis are expected. The most likely forecast is 9 orders. All will be purpose-built hulls. Most will be directly ordered by Þ eld operators, a few will be ordered by leasing contractors or midstream companies. Construction contract value is estimated in the area of $12 billion.Production spars ? Orders for 5 to 10 spars are expected. The most likely forecast is 8 orders. All will be purpose-built. Most will be directly ordered by Þ eld operators, a few will be ordered by midstream companies. Construction contract value is estimated around $7 billion.TLPs ? Orders for 4 to 6 TLPs are expected, with the most likely forecast being 5 orders. All will be purpose-built. Most, if not all, will be directly ordered by Þ eld operators. Construction contract value is estimated to be in the area of $6 billion. FLNGs ? Orders for 2 to 10 FLNGs are possible. Most likely forecast is 8 orders. The wide forecast range re ß ects tech- nical and commercial issues still to be resolved. Construction cost is likely in the range of $25 billion, but could be much higher or lower. FSRUs ? Orders for 15 to 23 FSRUs are likely. The most likely forecast is 20 orders. This is a rapidly expanding market sector. Construction cost is estimated in the area of $5 billion, but could be much higher. FSOs ? Orders for 25 to 35 FSOs are expected, with the most likely forecast being 30 orders. Around 33 percent will be purpose-built units. The remainder will be based on converted tanker hulls. Total construction cost is estimated around $4 billion.Source: IMA MR #9 (58-65).indd 64MR #9 (58-65).indd 648/30/2013 10:07:01 AM8/30/2013 10:07:01 AM