Page 10: of Offshore Engineer Magazine (Jan/Feb 2023)

Read this page in Pdf, Flash or Html5 edition of Jan/Feb 2023 Offshore Engineer Magazine

9

9

11

11

MARKETS THE RIG MARKET

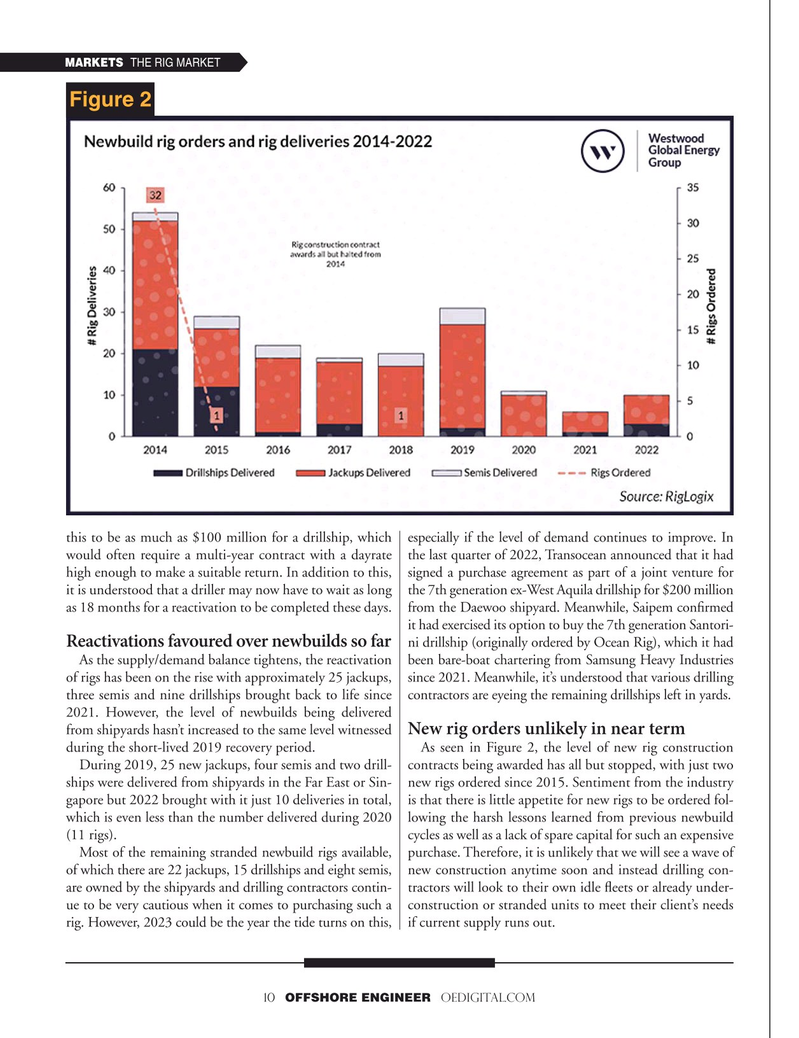

Figure 2 this to be as much as $100 million for a drillship, which especially if the level of demand continues to improve. In would often require a multi-year contract with a dayrate the last quarter of 2022, Transocean announced that it had high enough to make a suitable return. In addition to this, signed a purchase agreement as part of a joint venture for it is understood that a driller may now have to wait as long the 7th generation ex-West Aquila drillship for $200 million as 18 months for a reactivation to be completed these days. from the Daewoo shipyard. Meanwhile, Saipem con?rmed it had exercised its option to buy the 7th generation Santori- ni drillship (originally ordered by Ocean Rig), which it had

Reactivations favoured over newbuilds so far

As the supply/demand balance tightens, the reactivation been bare-boat chartering from Samsung Heavy Industries of rigs has been on the rise with approximately 25 jackups, since 2021. Meanwhile, it’s understood that various drilling three semis and nine drillships brought back to life since contractors are eyeing the remaining drillships left in yards. 2021. However, the level of newbuilds being delivered from shipyards hasn’t increased to the same level witnessed

New rig orders unlikely in near term during the short-lived 2019 recovery period. As seen in Figure 2, the level of new rig construction

During 2019, 25 new jackups, four semis and two drill- contracts being awarded has all but stopped, with just two ships were delivered from shipyards in the Far East or Sin- new rigs ordered since 2015. Sentiment from the industry gapore but 2022 brought with it just 10 deliveries in total, is that there is little appetite for new rigs to be ordered fol- which is even less than the number delivered during 2020 lowing the harsh lessons learned from previous newbuild (11 rigs). cycles as well as a lack of spare capital for such an expensive

Most of the remaining stranded newbuild rigs available, purchase. Therefore, it is unlikely that we will see a wave of of which there are 22 jackups, 15 drillships and eight semis, new construction anytime soon and instead drilling con- are owned by the shipyards and drilling contractors contin- tractors will look to their own idle ?eets or already under- ue to be very cautious when it comes to purchasing such a construction or stranded units to meet their client’s needs rig. However, 2023 could be the year the tide turns on this, if current supply runs out. 10 OFFSHORE ENGINEER OEDIGITAL.COM