Page 23: of Offshore Engineer Magazine (Mar/Apr 2024)

Read this page in Pdf, Flash or Html5 edition of Mar/Apr 2024 Offshore Engineer Magazine

22

22

24

24

MARKETS EXPLORATION industry will mainly target Scope 1 and Scope 2 emissions

Upstream Commitments Towards a Net Zero Future

Over 83% of companies we are tracking across the – only 14% of companies with net-zero commitments are upstream sector have established greenhouse gas (GHG) targeting Scope 3 emissions.

emissions reduction targets. The number will rise as

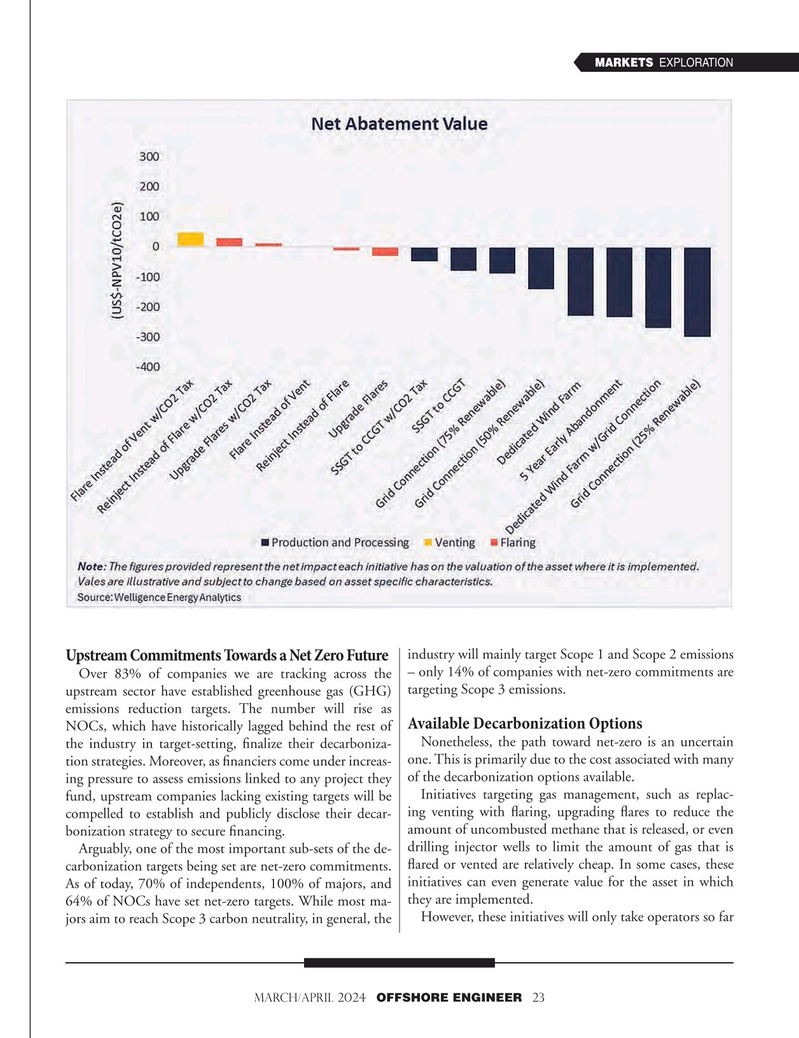

Available Decarbonization Options

NOCs, which have historically lagged behind the rest of

Nonetheless, the path toward net-zero is an uncertain the industry in target-setting, fnalize their decarboniza- one. This is primarily due to the cost associated with many tion strategies. Moreover, as fnanciers come under increas- ing pressure to assess emissions linked to any project they of the decarbonization options available.

Initiatives targeting gas management, such as replac- fund, upstream companies lacking existing targets will be ing venting with faring, upgrading fares to reduce the compelled to establish and publicly disclose their decar- amount of uncombusted methane that is released, or even bonization strategy to secure fnancing.

drilling injector wells to limit the amount of gas that is

Arguably, one of the most important sub-sets of the de- carbonization targets being set are net-zero commitments. fared or vented are relatively cheap. In some cases, these

As of today, 70% of independents, 100% of majors, and initiatives can even generate value for the asset in which they are implemented. 64% of NOCs have set net-zero targets. While most ma-

However, these initiatives will only take operators so far jors aim to reach Scope 3 carbon neutrality, in general, the

MARCH/APRIL 2024 OFFSHORE ENGINEER 23