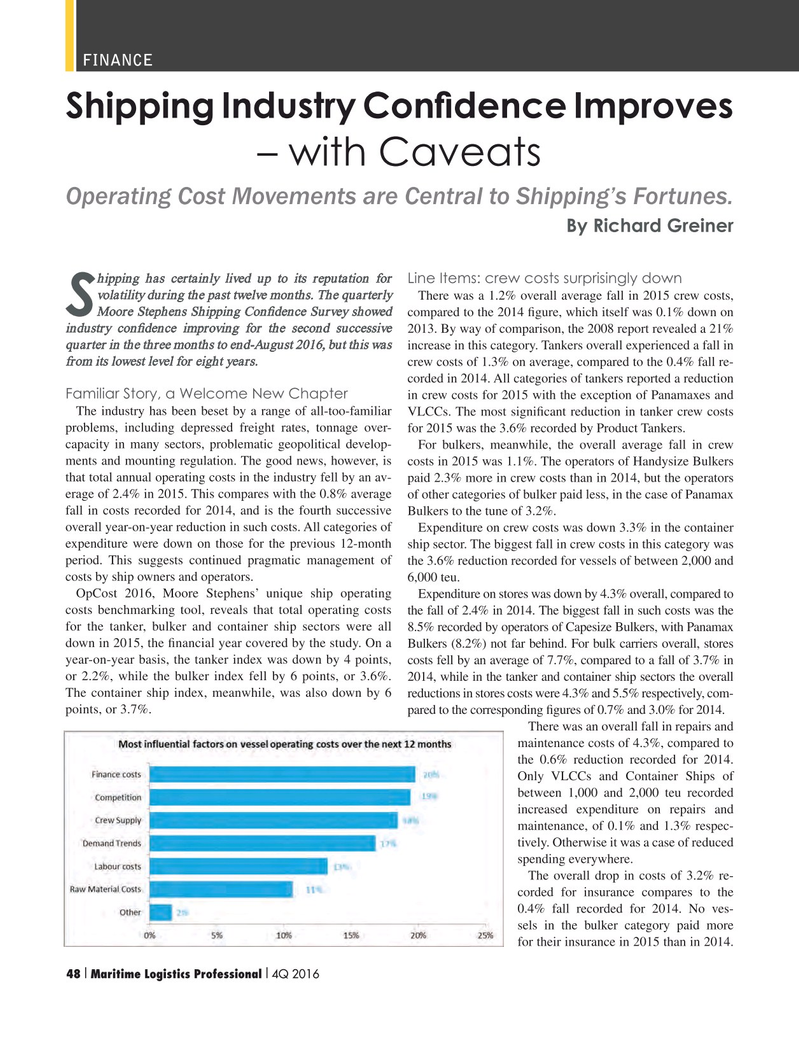

Page 48: of Maritime Logistics Professional Magazine (Q4 2016)

Workboats

Read this page in Pdf, Flash or Html5 edition of Q4 2016 Maritime Logistics Professional Magazine

47

47

49

49

FINANCE

Shipping Industry Con? dence Improves – with Caveats

Operating Cost Movements are Central to Shipping’s Fortunes.

By Richard Greiner hipping has certainly lived up to its reputation for

Line Items: crew costs surprisingly down volatility during the past twelve months. The quarterly There was a 1.2% overall average fall in 2015 crew costs,

SMoore Stephens Shipping Con? dence Survey showed compared to the 2014 ? gure, which itself was 0.1% down on industry con? dence improving for the second successive 2013. By way of comparison, the 2008 report revealed a 21% quarter in the three months to end-August 2016, but this was increase in this category. Tankers overall experienced a fall in from its lowest level for eight years. crew costs of 1.3% on average, compared to the 0.4% fall re- corded in 2014. All categories of tankers reported a reduction

Familiar Story, a Welcome New Chapter in crew costs for 2015 with the exception of Panamaxes and

The industry has been beset by a range of all-too-familiar VLCCs. The most signi? cant reduction in tanker crew costs problems, including depressed freight rates, tonnage over- for 2015 was the 3.6% recorded by Product Tankers.

capacity in many sectors, problematic geopolitical develop- For bulkers, meanwhile, the overall average fall in crew ments and mounting regulation. The good news, however, is costs in 2015 was 1.1%. The operators of Handysize Bulkers that total annual operating costs in the industry fell by an av- paid 2.3% more in crew costs than in 2014, but the operators erage of 2.4% in 2015. This compares with the 0.8% average of other categories of bulker paid less, in the case of Panamax fall in costs recorded for 2014, and is the fourth successive Bulkers to the tune of 3.2%.

overall year-on-year reduction in such costs. All categories of Expenditure on crew costs was down 3.3% in the container expenditure were down on those for the previous 12-month ship sector. The biggest fall in crew costs in this category was period. This suggests continued pragmatic management of the 3.6% reduction recorded for vessels of between 2,000 and costs by ship owners and operators. 6,000 teu.

OpCost 2016, Moore Stephens’ unique ship operating Expenditure on stores was down by 4.3% overall, compared to costs benchmarking tool, reveals that total operating costs the fall of 2.4% in 2014. The biggest fall in such costs was the for the tanker, bulker and container ship sectors were all 8.5% recorded by operators of Capesize Bulkers, with Panamax down in 2015, the ? nancial year covered by the study. On a Bulkers (8.2%) not far behind. For bulk carriers overall, stores year-on-year basis, the tanker index was down by 4 points, costs fell by an average of 7.7%, compared to a fall of 3.7% in or 2.2%, while the bulker index fell by 6 points, or 3.6%. 2014, while in the tanker and container ship sectors the overall

The container ship index, meanwhile, was also down by 6 reductions in stores costs were 4.3% and 5.5% respectively, com- points, or 3.7%. pared to the corresponding ? gures of 0.7% and 3.0% for 2014.

There was an overall fall in repairs and maintenance costs of 4.3%, compared to the 0.6% reduction recorded for 2014.

Only VLCCs and Container Ships of between 1,000 and 2,000 teu recorded increased expenditure on repairs and maintenance, of 0.1% and 1.3% respec- tively. Otherwise it was a case of reduced spending everywhere.

The overall drop in costs of 3.2% re- corded for insurance compares to the 0.4% fall recorded for 2014. No ves- sels in the bulker category paid more for their insurance in 2015 than in 2014. 48 Maritime Logistics Professional 4Q 2016I I 34-49 Q4 MP2016.indd 48 11/9/2016 12:27:51 PM