Page 24: of Maritime Reporter Magazine (May 15, 1980)

Read this page in Pdf, Flash or Html5 edition of May 15, 1980 Maritime Reporter Magazine

23

23

25

25

U.S. Shipbuilding Market (continued from page 25) nates the market. Effective operation in this market requires a clear understanding of the national maritime policy. In the United

States the policy is represented by the Mer- chant Marine Act of 1936 as amended in 1970, the 1916 Shipping Act, The Jones Act for Domestic Ships, the Public Law 664 which provides government-impelled cargo preference, and other legislation. In the ab- sence of clear policy direction and implemen- tation of responsive maritime laws by all the Government departments involved, the

United States does not have an effective maritime policy at this time.

Various new provisions are being proposed by the maritime industry, including bilateral trade agreements or other cargo-sharing agreements, tax incentives, and less restric- tion on the operations of U.S. ships in world- wide and domestic trading. In terms of planning and organizing the industry's op- erations, reasonable foreknowledge of the

Government's position is almost more im- portant than the exact form which the as- sistance may take.

Military Market

The U.S. military shipbuilding market can be divided into four basic markets: U.S.

Navy; U.S. Coast Guard; U.S. Army, and foreign military sales.

Most major U.S. yards have maintained a naval shipbuilding capability to support their workforce during periods of low de- mand for commercial ships. In fact many

U.S. yards rely heavily on the military ship- building market. About 70 percent of the dollar value of major U.S. shipbuilding is naval construction.

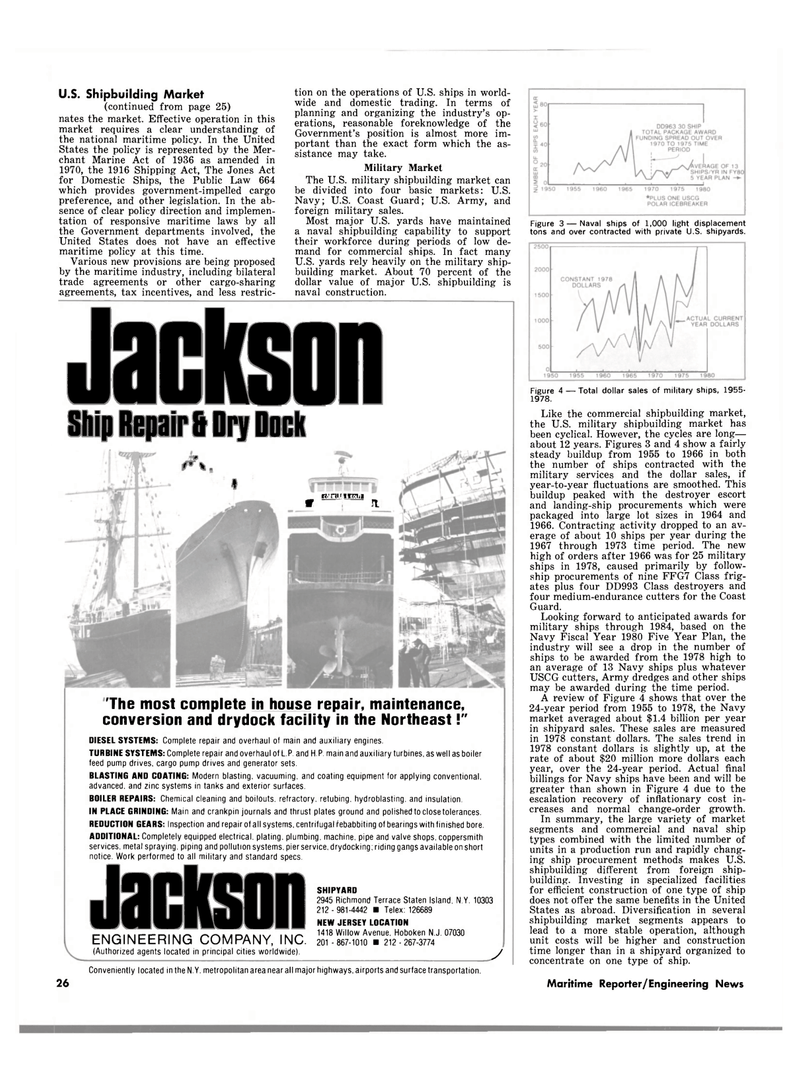

Figure 3 — Naval ships of 1,000 light displacement tons and over contracted with private U.S. shipyards.

Figure 4 — Total dollar sales of military ships, 1955- 1978.

Like the commercial shipbuilding market, the U.S. military shipbuilding market has been cyclical. However, the cycles are long— about 12 years. Figures 3 and 4 show a fairly steady buildup from 1955 to 1966 in both the number of ships contracted with the military services and the dollar sales, if year-to-year fluctuations are smoothed. This buildup peaked with the destroyer escort and landing-ship procurements which were packaged into large lot sizes in 1964 and 1966. Contracting activity dropped to an av- erage of about 10 ships per year during the 1967 through 1973 time period. The new high of orders after 1966 was for 25 military ships in 1978, caused primarily by fellow- ship procurements of nine FFG7 Class frig- ates plus four DD993 Class destroyers and four medium-endurance cutters for the Coast

Guard.

Looking forward to anticipated awards for military ships through 1984, based on the

Navy Fiscal Year 1980 Five Year Plan, the industry will see a drop in the number of ships to be awarded from the 1978 high to an average of 13 Navy ships plus whatever

USCG cutters, Army dredges and other ships may be awarded during the time period.

A review of Figure 4 shows that over the 24-year period from 1955 to 1978, the Navy market averaged about $1.4 billion per year in shipyard sales. These sales are measured in 1978 constant dollars. The sales trend in 1978 constant dollars is slightly up, at the rate of about $20 million more dollars each year, over the 24-year period. Actual final billings for Navy ships have been and will be greater than shown in Figure 4 due to the escalation recovery of inflationary cost in- creases and normal change-order growth.

In summary, the large variety of market segments and commercial and naval ship types combined with the limited number of units in a production run and rapidly chang- ing ship procurement methods makes U.S. shipbuilding different from foreign ship- building. Investing in specialized facilities for efficient construction of one type of ship does not offer the same benefits in the United

States as abroad. Diversification in several shipbuilding market segments appears to lead to a more stable operation, although unit costs will be higher and construction time longer than in a shipyard organized to concentrate on one type of ship.

ZIDELL Maritime Reporter/Engineering News 'The most complete in house repair, maintenance, conversion and drydock facility in the Northeast!"

DIESEL SYSTEMS: Complete repair and overhaul of main and auxiliary engines.

TURBINE SYSTEMS: Complete repair and overhaul of LP. and H P. main and auxiliary turbines, as well as boiler feed pump drives, cargo pump drives and generator sets.

BLASTING AND COATING: Modern blasting, vacuuming, and coating equipment for applying conventional, advanced, and zinc systems in tanks and exterior surfaces.

BOILER REPAIRS: Chemical cleaning and boilouts. refractory, retubing. hydroblasting. and insulation.

IN PLACE GRINDING: Main and crankpin journals and thrust plates ground and polished to close tolerances.

REDUCTION GEARS: Inspection and repair of all systems, centrifugal febabbiting of bearings with finished bore.

ADDITIONAL: Completely equipped electrical, plating, plumbing, machine, pipe and valve shops, coppersmith services, metal spraying, piping and pollution systems, pier service, drydocking; riding gangs available on short notice. Work performed to all military and standard specs. Jackson

SHIPYARD 2945 Richmond Terrace Staten Island, N.Y. 10303 212 - 981-4442 • Telex: 126689

NEW JERSEY LOCATION r-M/^iMi-r-niM^ ^ ^ i * i-> a k , i m1418 Willow Avenue, Hoboken N.J. 07030 ENGINEERING COMPANY, INC. 201 -867-1010 • 212-257-3774 (Authorized agents located in principal cities worldwide). y

Conveniently located in the N.Y. metropolitan area near all major highways, airports and surface transportation. 26

Jackson

Ship Repair & Dry Dock rV ft

H.1;

W ft