Page 20: of Offshore Engineer Magazine (Jul/Aug 2013)

Read this page in Pdf, Flash or Html5 edition of Jul/Aug 2013 Offshore Engineer Magazine

19

19

21

21

returns when up-front exploration costs taken on similarly large positions. weaker opportunities. are material. Third, the lack of existing This amount of new frontier acreage Other deals will be driven by the infrastructure often results in high devel- would normally command extensive exploration minnows. The biggest opment costs. Lastly, companies invest- drilling programs. A conservative esti- hurdle for this group is always access ing in frontier basins generally have no mate suggests that the Majors’ post-2010 to capital. Even when the capital mar- existing production revenues for early acreage alone might merit some 200 kets are at their most supportive, many

Perspectives recovery of exploration costs. Offsetting high-impact wells with a total explora- small cap explorers rely on promoted some of these negatives, fscal terms are tion investment of about US$40 billion. deals to carry them through a large part usually more attractive in frontier prov- of their drilling costs. Their recent fron- inces. Average government take is 58% tier land-grab has redoubled this issue.

Exploration well in frontier basins, a full 5% lower than First, there are now an unusually large success rate (2002-2011) in mature basins. Governments offer number of such companies seeking fund- 60% more attractive terms to entice inves- ing. Second, much of their new acreage tors and reward them for the high level includes plays that will be expensive 50% of risk they are assuming. Once a basin to drill.

is de-risked, there is often a rebalancing The expanded requirement for fund- 40% of the risk-reward equation, with terms ing coincides with a period of market 30% becoming more onerous. nervousness. Investors have a dimin-

Although the economics of frontier ished appetite for the broader oil and gas 20% exploration are more challenging, they sector, which has underperformed over are nonetheless positive, and we have the past year. Exposure to pure explora- 10% seen a shift in the spending patterns of tion risk is particularly out of market the most successful explorers toward favor. It is clear that the small caps 0% frontier and emerging basins. That collectively hold far more acreage than

BP

Eni

Shell

Total shift has come at a time of increasing they can reasonably explore. Those that

Statoil

Chevron exploration expenditure; more is being have insuffcient production revenue to

ExxonMobil

Overall success rate spent on frontier exploration than ever be self-funding will seek larger partners,

Commercial success rate before. The Independents are, relative especially when looming drill-or-drop

Average frontier overall success rate to their size, spending more on explora- decisions move them to partially divest,

Average frontier commercial success rate tion than the Majors. Most Majors are rather than fully relinquish acreage.

Source: Wood Mackenzie spending US$2–3/bbl of production, Companies that continue to focus while Independents typically spend Clearly, neither the Majors nor the small on high-impact conventional explora- two to three times that amount. Shell caps have binding commitments to tion will welcome the enhanced fow and Statoil have hiked their exploration explore or invest at anything like these of frontier opportunities. Likely buyers spending over the past few years to reach levels. We believe there will be a new include well-funded and technically- levels above US$5/boe of production. If wave of frontier exploration deals. strong Independents. Many look well-

ExxonMobil, BP, and Chevron were to Some deals will be driven by the positioned to enhance their portfolios. increase their expenditure to the $5/boe Majors. They have added more prospect We may even see some divestments of mark, an additional US$12 billion would acreage than can be realistically tested, predevelopment assets, as strong explor- be spent on exploration each year. and will farm-out selectively. High- ers reposition on wildcatting.

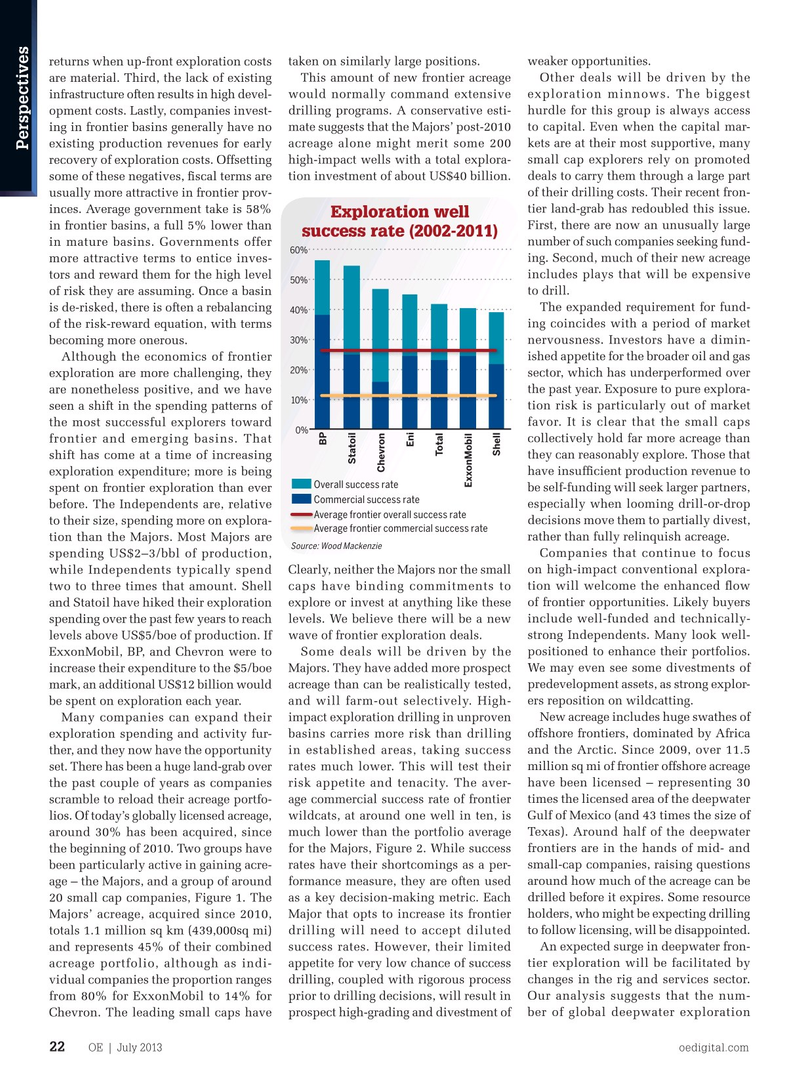

Many companies can expand their impact exploration drilling in unproven New acreage includes huge swathes of exploration spending and activity fur- basins carries more risk than drilling offshore frontiers, dominated by Africa ther, and they now have the opportunity in established areas, taking success and the Arctic. Since 2009, over 11.5 set. There has been a huge land-grab over rates much lower. This will test their million sq mi of frontier offshore acreage the past couple of years as companies risk appetite and tenacity. The aver- have been licensed – representing 30 scramble to reload their acreage portfo- age commercial success rate of frontier times the licensed area of the deepwater lios. Of today’s globally licensed acreage, wildcats, at around one well in ten, is Gulf of Mexico (and 43 times the size of around 30% has been acquired, since much lower than the portfolio average Texas). Around half of the deepwater the beginning of 2010. Two groups have for the Majors, Figure 2. While success frontiers are in the hands of mid- and been particularly active in gaining acre- rates have their shortcomings as a per- small-cap companies, raising questions age – the Majors, and a group of around formance measure, they are often used around how much of the acreage can be 20 small cap companies, Figure 1. The as a key decision-making metric. Each drilled before it expires. Some resource

Majors’ acreage, acquired since 2010, Major that opts to increase its frontier holders, who might be expecting drilling totals 1.1 million sq km (439,000sq mi) drilling will need to accept diluted to follow licensing, will be disappointed.

and represents 45% of their combined success rates. However, their limited An expected surge in deepwater fron- acreage portfolio, although as indi- appetite for very low chance of success tier exploration will be facilitated by vidual companies the proportion ranges drilling, coupled with rigorous process changes in the rig and services sector. from 80% for ExxonMobil to 14% for prior to drilling decisions, will result in Our analysis suggests that the num-

Chevron. The leading small caps have prospect high-grading and divestment of ber of global deepwater exploration

OE | July 2013 oedigital.com 22

Analysis_WoodMac_Quickstats.indd 22 6/24/13 1:47 AM