Page 15: of Maritime Logistics Professional Magazine (Q2 2014)

Maritime Risk & Shipping Finance

Read this page in Pdf, Flash or Html5 edition of Q2 2014 Maritime Logistics Professional Magazine

14

14

16

16

” “

Financial Risk and M&A Deals

Financial transactions, particularly large ones, involve a complex and in-depth evaluation of risks by players on both sides of the deal. In Mergers and Acquisitions, sellers gener- ally seek to diversify their portfolios by reducing their expo- sure to the risk of holding ownership in the subject company.

Meanwhile, the buyer and its advisors expend often enormous time and resources in the analysis of the risks they are taking on during the “due diligence” period.

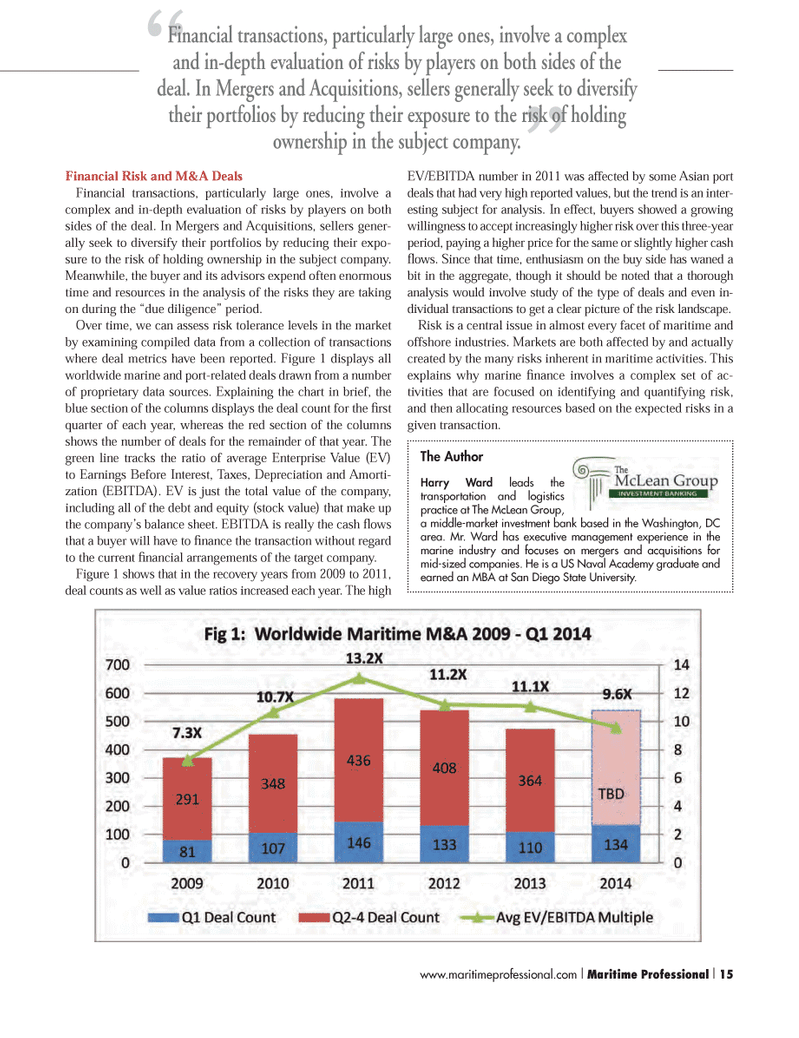

Over time, we can assess risk tolerance levels in the market by examining compiled data from a collection of transactions where deal metrics have been reported. Figure 1 displays all worldwide marine and port-related deals drawn from a number of proprietary data sources. Explaining the chart in brief, the blue section of the columns displays the deal count for the fi rst quarter of each year, whereas the red section of the columns shows the number of deals for the remainder of that year. The green line tracks the ratio of average Enterprise Value (EV) to Earnings Before Interest, Taxes, Depreciation and Amorti- zation (EBITDA). EV is just the total value of the company, including all of the debt and equity (stock value) that make up the company’s balance sheet. EBITDA is really the cash fl ows that a buyer will have to fi nance the transaction without regard to the current fi nancial arrangements of the target company.

Figure 1 shows that in the recovery years from 2009 to 2011, deal counts as well as value ratios increased each year. The high

EV/EBITDA number in 2011 was affected by some Asian port deals that had very high reported values, but the trend is an inter- esting subject for analysis. In effect, buyers showed a growing willingness to accept increasingly higher risk over this three-year period, paying a higher price for the same or slightly higher cash fl ows. Since that time, enthusiasm on the buy side has waned a bit in the aggregate, though it should be noted that a thorough analysis would involve study of the type of deals and even in- dividual transactions to get a clear picture of the risk landscape.

Risk is a central issue in almost every facet of maritime and offshore industries. Markets are both affected by and actually created by the many risks inherent in maritime activities. This explains why marine fi nance involves a complex set of ac- tivities that are focused on identifying and quantifying risk, and then allocating resources based on the expected risks in a given transaction.

Financial transactions, particularly large ones, involve a complex and in-depth evaluation of risks by players on both sides of the deal. In Mergers and Acquisitions, sellers generally seek to diversify their portfolios by reducing their exposure to the risk of holding ownership in the subject company.

The Author

Harry Ward leads the transportation and logistics practice at The McLean Group, a middle-market investment bank based in the Washington, DC area. Mr. Ward has executive management experience in the marine industry and focuses on mergers and acquisitions for mid-sized companies. He is a US Naval Academy graduate and earned an MBA at San Diego State University. www.maritimeprofessional.com I Maritime Professional I 15 1-17 Q2 MP2014.indd 15 5/16/2014 11:42:54 AM