Page 18: of Maritime Reporter Magazine (August 2012)

The Shipyard Edition

Read this page in Pdf, Flash or Html5 edition of August 2012 Maritime Reporter Magazine

17

17

19

19

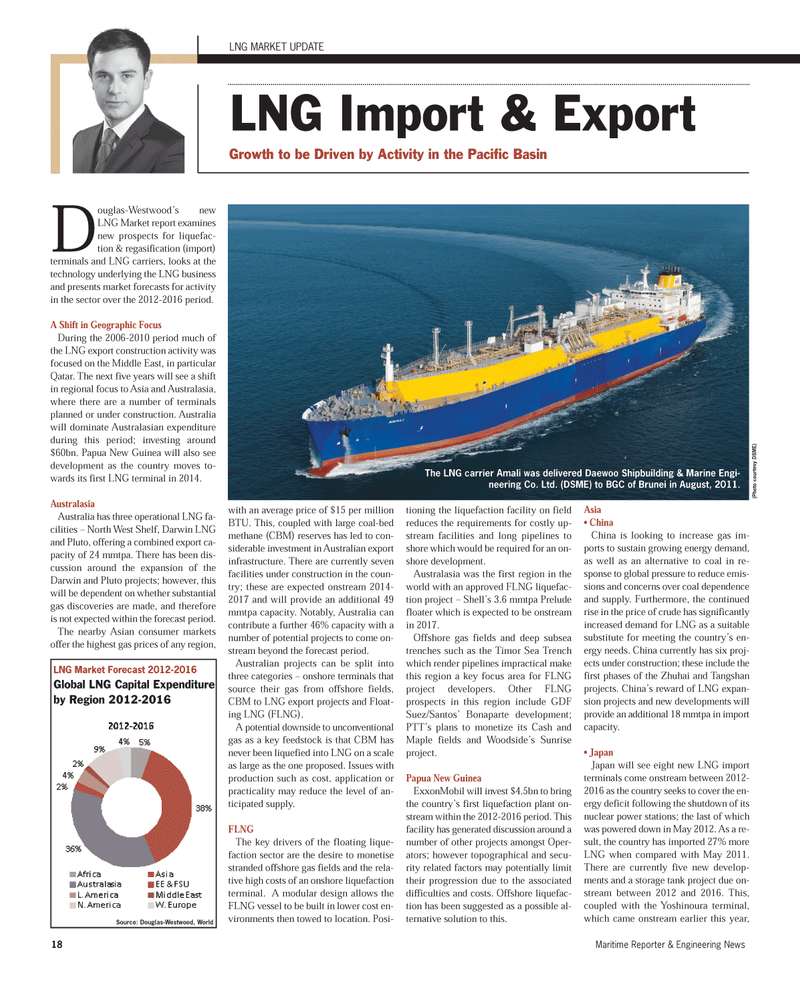

18Maritime Reporter & Engineering News Douglas-Westwood?s new LNG Market report examines new prospects for liquefac- tion & regasification (import) terminals and LNG carriers, looks at thetechnology underlying the LNG business and presents market forecasts for activity in the sector over the 2012-2016 period. A Shift in Geographic Focus During the 2006-2010 period much ofthe LNG export construction activity was focused on the Middle East, in particularQatar. The next five years will see a shift in regional focus to Asia and Australasia, where there are a number of terminalsplanned or under construction. Australia will dominate Australasian expenditure during this period; investing around $60bn. Papua New Guinea will also see development as the country moves to- wards its first LNG terminal in 2014. Australasia Australia has three operational LNG fa- cilities ? North West Shelf, Darwin LNG and Pluto, offering a combined export ca- pacity of 24 mmtpa. There has been dis- cussion around the expansion of the Darwin and Pluto projects; however, this will be dependent on whether substantialgas discoveries are made, and therefore is not expected within the forecast period. The nearby Asian consumer markets offer the highest gas prices of any region, with an average price of $15 per million BTU. This, coupled with large coal-bed methane (CBM) reserves has led to con- siderable investment in Australian export infrastructure. There are currently seven facilities under construction in the coun- try; these are expected onstream 2014- 2017 and will provide an additional 49 mmtpa capacity. Notably, Australia can contribute a further 46% capacity with a number of potential projects to come on-stream beyond the forecast period. Australian projects can be split intothree categories ? onshore terminals that source their gas from offshore fields, CBM to LNG export projects and Float- ing LNG (FLNG).A potential downside to unconventional gas as a key feedstock is that CBM has never been liquefied into LNG on a scale as large as the one proposed. Issues with production such as cost, application orpracticality may reduce the level of an- ticipated supply. FLNGThe key drivers of the floating lique- faction sector are the desire to monetise stranded offshore gas fields and the rela- tive high costs of an onshore liquefaction terminal. A modular design allows the FLNG vessel to be built in lower cost en- vironments then towed to location. Posi- tioning the liquefaction facility on field reduces the requirements for costly up-stream facilities and long pipelines to shore which would be required for an on- shore development. Australasia was the first region in the world with an approved FLNG liquefac- tion project ? Shell?s 3.6 mmtpa Prelude floater which is expected to be onstream in 2017. Offshore gas fields and deep subsea trenches such as the Timor Sea Trench which render pipelines impractical make this region a key focus area for FLNG project developers. Other FLNG prospects in this region include GDF Suez/Santos? Bonaparte development; PTT?s plans to monetize its Cash and Maple fields and Woodside?s Sunrise project.Papua New Guinea ExxonMobil will invest $4.5bn to bring the country?s first liquefaction plant on- stream within the 2012-2016 period. This facility has generated discussion around a number of other projects amongst Oper- ators; however topographical and secu- rity related factors may potentially limit their progression due to the associateddifficulties and costs. Offshore liquefac- tion has been suggested as a possible al-ternative solution to this. Asia ChinaChina is looking to increase gas im- ports to sustain growing energy demand, as well as an alternative to coal in re- sponse to global pressure to reduce emis-sions and concerns over coal dependence and supply. Furthermore, the continued rise in the price of crude has significantly increased demand for LNG as a suitablesubstitute for meeting the country?s en- ergy needs. China currently has six proj- ects under construction; these include thefirst phases of the Zhuhai and Tangshan projects. China?s reward of LNG expan- sion projects and new developments will provide an additional 18 mmtpa in import capacity. Japan Japan will see eight new LNG import terminals come onstream between 2012-2016 as the country seeks to cover the en- ergy deficit following the shutdown of its nuclear power stations; the last of which was powered down in May 2012. As a re- sult, the country has imported 27% moreLNG when compared with May 2011.There are currently five new develop- ments and a storage tank project due on-stream between 2012 and 2016. This, coupled with the Yoshinoura terminal, which came onstream earlier this year, LNG MARKET UPDATE LNG Import & ExportGrowth to be Driven by Activity in the Pacific Basin The LNG carrier Amali was delivered Daewoo Shipbuilding & Marine Engi- neering Co. Ltd. (DSME) to BGC of Brunei in August, 2011.(Photo courtesy DSME) LNG Market Forecast 2012-2016 Global LNG Capital Expenditure by Region 2012-2016Source: Douglas-Westwood, World MR#8 (18-25):MR Template 8/8/2012 11:07 AM Page 18