Page 20: of Maritime Reporter Magazine (August 2012)

The Shipyard Edition

Read this page in Pdf, Flash or Html5 edition of August 2012 Maritime Reporter Magazine

19

19

21

21

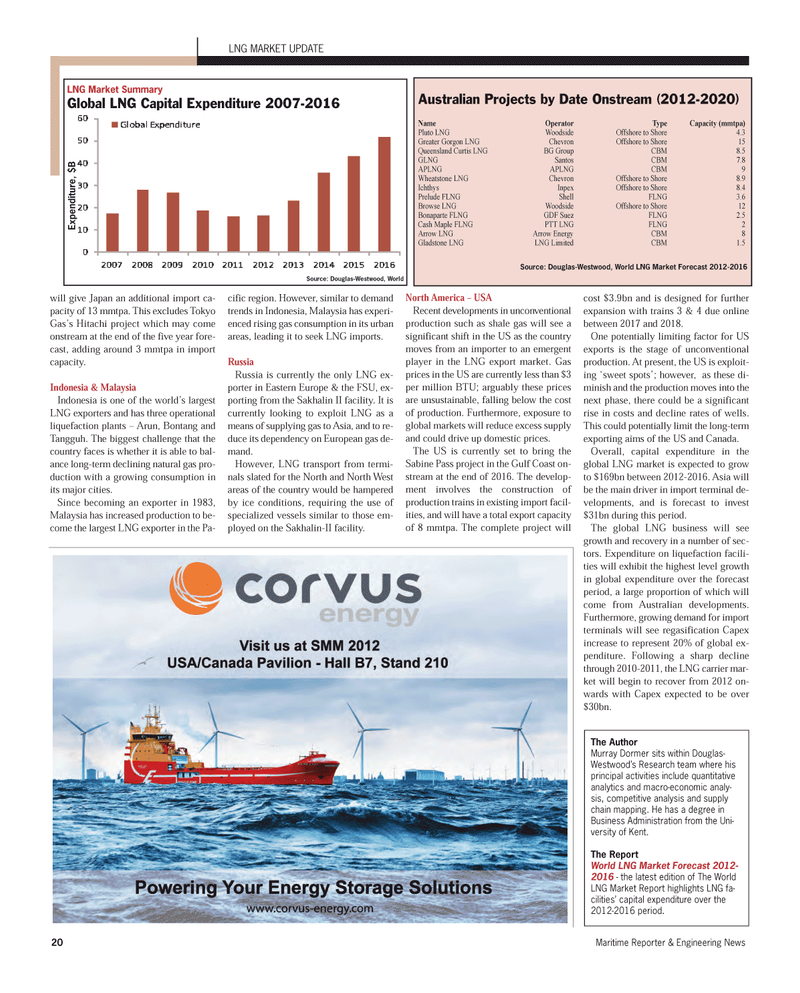

20Maritime Reporter & Engineering News will give Japan an additional import ca- pacity of 13 mmtpa. This excludes Tokyo Gas?s Hitachi project which may come onstream at the end of the five year fore- cast, adding around 3 mmtpa in importcapacity. Indonesia & Malaysia Indonesia is one of the world?s largest LNG exporters and has three operational liquefaction plants ? Arun, Bontang and Tangguh. The biggest challenge that the country faces is whether it is able to bal- ance long-term declining natural gas pro- duction with a growing consumption in its major cities.Since becoming an exporter in 1983, Malaysia has increased production to be-come the largest LNG exporter in the Pa- cific region. However, similar to demand trends in Indonesia, Malaysia has experi- enced rising gas consumption in its urban areas, leading it to seek LNG imports. RussiaRussia is currently the only LNG ex- porter in Eastern Europe & the FSU, ex- porting from the Sakhalin II facility. It is currently looking to exploit LNG as a means of supplying gas to Asia, and to re- duce its dependency on European gas de- mand. However, LNG transport from termi- nals slated for the North and North West areas of the country would be hampered by ice conditions, requiring the use ofspecialized vessels similar to those em- ployed on the Sakhalin-II facility. North America ? USA Recent developments in unconventional production such as shale gas will see a significant shift in the US as the country moves from an importer to an emergent player in the LNG export market. Gas prices in the US are currently less than $3per million BTU; arguably these prices are unsustainable, falling below the cost of production. Furthermore, exposure to global markets will reduce excess supply and could drive up domestic prices. The US is currently set to bring theSabine Pass project in the Gulf Coast on- stream at the end of 2016. The develop- ment involves the construction of production trains in existing import facil- ities, and will have a total export capacity of 8 mmtpa. The complete project will cost $3.9bn and is designed for furtherexpansion with trains 3 & 4 due online between 2017 and 2018.One potentially limiting factor for US exports is the stage of unconventional production. At present, the US is exploit- ing ?sweet spots?; however, as these di- minish and the production moves into the next phase, there could be a significant rise in costs and decline rates of wells.This could potentially limit the long-termexporting aims of the US and Canada. Overall, capital expenditure in the global LNG market is expected to grow to $169bn between 2012-2016. Asia will be the main driver in import terminal de- velopments, and is forecast to invest $31bn during this period. The global LNG business will see growth and recovery in a number of sec- tors. Expenditure on liquefaction facili- ties will exhibit the highest level growth in global expenditure over the forecast period, a large proportion of which will come from Australian developments. Furthermore, growing demand for import terminals will see regasification Capex increase to represent 20% of global ex- penditure. Following a sharp decline through 2010-2011, the LNG carrier mar- ket will begin to recover from 2012 on- wards with Capex expected to be over $30bn.Australian Projects by Date Onstream (2012-2020) NameOperatorTypeCapacity (mmtpa) Pluto LNG Woodside Offshore to Shore 4.3Greater Gorgon LNG ChevronOffshore to Shore 15Queensland Curtis LNG BG GroupCBM 8.5GLNGSantosCBM7.8APLNGAPLNGCBM9Wheatstone LNGChevronOffshore to Shore 8.9IchthysInpexOffshore to Shore 8.4Prelude FLNGShellFLNG3.6Browse LNGWoodside Offshore to Shore 12Bonaparte FLNGGDF SuezFLNG2.5Cash Maple FLNGPTT LNG FLNG2Arrow LNGArrow Energy CBM 8Gladstone LNGLNG LimitedCBM 1.5Source: Douglas-Westwood, World LNG Market Forecast 2012-2016 LNG MARKET UPDATE LNG Market SummaryGlobal LNG Capital Expenditure 2007-2016 Source: Douglas-Westwood, World The AuthorMurray Dormer sits within Douglas-Westwood?s Research team where his principal activities include quantitativeanalytics and macro-economic analy- sis, competitive analysis and supplychain mapping. He has a degree in Business Administration from the Uni- versity of Kent.The Report World LNG Market Forecast 2012- 2016- the latest edition of The World LNG Market Report highlights LNG fa- cilities? capital expenditure over the 2012-2016 period. Expenditure, $B MR#8 (18-25):MR Template 8/10/2012 4:26 PM Page 20