Page 16: of Offshore Engineer Magazine (Mar/Apr 2017)

Read this page in Pdf, Flash or Html5 edition of Mar/Apr 2017 Offshore Engineer Magazine

15

15

17

17

RIG MARKET REVIEW

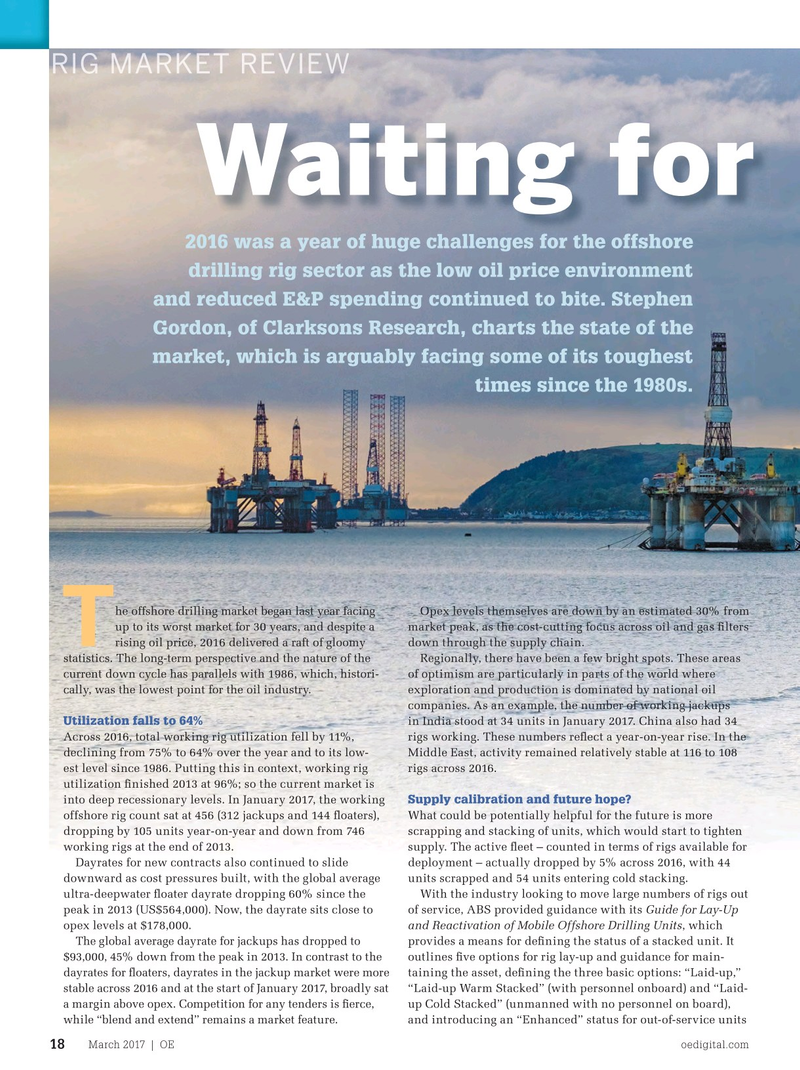

Waiting for the bright side 2016 was a year of huge challenges for the offshore drilling rig sector as the low oil price environment and reduced E&P spending continued to bite. Stephen

Gordon, of Clarksons Research, charts the state of the market, which is arguably facing some of its toughest times since the 1980s.

he offshore drilling market began last year facing Opex levels themselves are down by an estimated 30% from that indicates the unit has had its lay-up location up to its worst market for 30 years, and despite a market peak, as the cost-cutting focus across oil and gas ? lters and procedures reviewed to a higher standard

T rising oil price, 2016 delivered a raft of gloomy down through the supply chain. and veri? ed by ABS in accordance with the guide. statistics. The long-term perspective and the nature of the Regionally, there have been a few bright spots. These areas The guide also includes requirements for reactiva- current down cycle has parallels with 1986, which, histori- of optimism are particularly in parts of the world where tion that allows surveyors to verify that the unit cally, was the lowest point for the oil industry. exploration and production is dominated by national oil meets class standards to move onsite and begin companies. As an example, the number of working jackups operations.

Utilization falls to 64% in India stood at 34 units in January 2017. China also had 34 It is increasingly dif? cult to use the available data to track

Across 2016, total working rig utilization fell by 11%, rigs working. These numbers re? ect a year-on-year rise. In the the exact status of rigs and their ability declining from 75% to 64% over the year and to its low- Middle East, activity remained relatively stable at 116 to 108 to re-enter the market precisely, even for est level since 1986. Putting this in context, working rig rigs across 2016. assets that recently reached the end of a utilization ? nished 2013 at 96%; so the current market is drilling contract.

Supply calibration and future hope?

into deep recessionary levels. In January 2017, the working

Orderbook uncertainty offshore rig count sat at 456 (312 jackups and 144 ? oaters), What could be potentially helpful for the future is more dropping by 105 units year-on-year and down from 746 scrapping and stacking of units, which would start to tighten The status of the rig orderbook at ship- working rigs at the end of 2013. supply. The active ? eet – counted in terms of rigs available for yards remains largely uncertain. Numbers

Dayrates for new contracts also continued to slide deployment – actually dropped by 5% across 2016, with 44 generated from Clarksons’ data indicate downward as cost pressures built, with the global average units scrapped and 54 units entering cold stacking. that the rig orderbook for 2017 stands at ultra-deepwater ? oater dayrate dropping 60% since the With the industry looking to move large numbers of rigs out 164 units, with an aggregate original new- peak in 2013 (US$564,000). Now, the dayrate sits close to of service, ABS provided guidance with its Guide for Lay-Up build contract value of $60 billion.

opex levels at $178,000. and Reactivation of Mobile Offshore Drilling Units, which It is important to note that while there

The global average dayrate for jackups has dropped to provides a means for de? ning the status of a stacked unit. It are orders on the books, delivery dates $93,000, 45% down from the peak in 2013. In contrast to the outlines ? ve options for rig lay-up and guidance for main- remain uncertain. Nearly 60% of the dayrates for ? oaters, dayrates in the jackup market were more taining the asset, de? ning the three basic options: “Laid-up,” orderbook is largely constructed, but it is stable across 2016 and at the start of January 2017, broadly sat “Laid-up Warm Stacked” (with personnel onboard) and “Laid- very possible that these units will remain a margin above opex. Competition for any tenders is ? erce, up Cold Stacked” (unmanned with no personnel on board), in yards for some time and in some cases while “blend and extend” remains a market feature.

and introducing an “Enhanced” status for out-of-service units face an uncertain future entirely.

March 2017 | OE oedigital.com 18 018_OE0217_Feat1_ABS_v2.indd 18 2/21/17 5:01 PM