Lease Equipment

-

- Floating Production Roundup: August 2014 Maritime Reporter, Aug 2014 #32

What’s New in August 2014

There are 320 oil/gas floating production units are now in service, on order or available for reuse on another field. FPSOs account for 64% of the existing systems, 79% of systems on order. Production semis, barges, spars and TLPs comprise the balance. Total oil/gas inventory is the same as last month – but two units on order last month (N’Goma FPSO and Delta House Semi) were completed and are now in the active inventory.

Another 29 floating LNG processing systems are in service or on order. Liquefaction floaters account for 17%, regasification floaters 83%. No liquefaction floaters are yet in service – all five are on order. Total LNG inventory is the same as last month.

In addition, 102 floating storage units are in service, on order or available.

Production Floater Order Backlog

Sixty-three production floaters are currently on order, a reduction of two units since last month. The figure includes 37 FPSOs, 10 other oil/gas production units and 16 LNG processing units. In the later are five floating liquefaction plants and 11 regasification terminals.

The backlog of orders has been falling over the past few months as deliveries outpace intake. Backlog is down from a high of 72 units last October. Given expected orders and scheduled deliveries over the next five months, order backlog at end 2014 will likely be in the range of 58 to 60 units.

The declining trend is mostly the result of a wave of orders 24 to 36 months back that created a cluster of deliveries in 2014. Recent orders have been strong – just not as high as deliveries. But there has also been some impact from deferral/rethinking of several projects – e.g., Rosebank, Fram, Fyne, Mad Dog, Cheviot, etc.

Who’s Building What

Production and storage floaters are being built in more than 40 locations.

MR8 Offshore Floater NotesHere’s a summary of where various type systems are currently being built.

• FPSO conversions – Shipyards in Singapore and China are the principal players in this type activity. Of the 20 FPSO conversions now in progress, nine are being performed in Singapore. Keppel is converting six tankers to FPSOs, Sembawang is converting two tankers and Jurong has one conversion. Another eight conversions are being performed in China – three at Chengxi and five at Cosco Dalian. To meet local content requirements, a portion of topsides completion in around half of these contracts is being performed in Brazil.

• Purpose built FPSOs – Korea and Brazil are the main sources of large purpose built FPSOs. Yards in these countries have contracts for 13 of the 17 new FPSOs now on order. In Korea, Hyundai is building two FPSOs, Samsung two units and Daewoo one unit. One of the Samsung units (Egina) will have significant topsides work performed in Nigeria. In Brazil eight replica FPSOs are being built by Ecovix at the new Rio Grande Shipyard. Elsewhere, two FPSOs are being built in China and two FPSO hulls are being built in Japan with topsides finishing in Singapore or Brazil.

• Other oil/gas production units – Asia is the dominant area for building non-shipshape production units. At the moment five of the 10 large purpose-built non-shipshape units on order are being built in Korea. Samsung is building a production semi and Hyundai is building a spar, a TLP and two large production barges. The topsides to several units are being completed in the US or Indonesia. Elsewhere, a spar hull is being built in Finland for topsides completion in the US and MMHE is finishing a TLP in Malaysia.

• FSRUs – Construction of regas units is fully reserved to Korea and China. Eight FSRUs are now being built in Korea. Samsung is building four FSRUs, Hyundai and Daewoo are each building two FSRUs. In China, Wison Nantong is building two FSRU barges.

• FLNGs – Liquefaction floaters are all being built in Asia. In Korea, Samsung is building two units, including the massive Prelude FLNG for Shell and the initial FLNG for Petronas. Daewoo is building the second FLNG ordered by Petronas.

In China, Wison is building a liquefaction barge for use in Colombia. All of these units are newly built hulls. In Singapore, Keppel is converting an LNG carrier into an FLNG.

The large role of Asia facilities in this market sector is apparent from the above. Overall, 50 of the 63 current production floater orders are contracted with Asian yards.

In term of number of production floater fabrication/conversion contracts being performed, the Asian share of market is just under 80%.

Backlog of Planned Floater Projects

231 floating production projects are in various stages of planning as of beginning August. Of these, 58% involve an FPSO, 13% another type oil/gas production floater, 23% liquefaction or regasification floater and 6% storage/offloading floater.

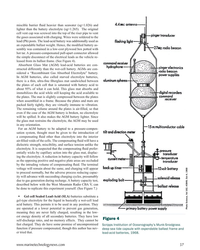

Among new projects emerging since last month, LoneStar FLNG, a Texas company, proposes to build an FLNG by inserting a midsection in an existing Moss LNG carrier. The mid-section would contain the liquefaction module and turret. Processing and gas treatment would be on an accompanying cylindrical FPSO or fixed platform. The unit would be capable of processing 1 to 4 mtpa. LNG transfer from the FLNG to transport carrier would be performed in a sheltered area. Among proposed applications is use of the unit for gas export in the US GOM.

Brazil, Africa and SE Asia continue to be the major locations of floating production projects in the visible planning stage. We are tracking 44 projects in Brazil, 50 in Africa and 40 projects in SEA – 58% of the visible planned floating production projects worldwide. Several large projects in Brazil and (less so) Africa will require multiple production units.

Around 12% of the 231 visible planned projects are likely to advance to the EPC contracting stage within the next 12 to 18 months. These projects typically have either entered the FEED phase, prequalification of floater contractors has been initiated or bidding/negotiation is in progress. A list of near term projects is provided below.

Another 50% of the visible projects are at a stage of development where the EPC contract for the production unit is likely within the next 18 to 48 months. The remaining 38% of projects are less advanced in planning, with the EPC contract likely four to 10 years out.

Outlook for Equipment Orders

Oil demand keeps growing, the threat of conventional supply disruption keeps pressure on finding new sources of oil and a large number of additional deepwater drill rigs are entering service. These are clearly positive indicators for deepwater project starts and floating production system orders.

Importantly, the most basic underlying market driver, price of crude oil, remains supportive of deepwater oil development. As of beginning August, Brent is trading around $106. For delivery at the end the decade, Brent is trading around $99 in the futures market. This pricing level provides solid commercial support to all but the most marginal deepwater projects.

But oil companies have been pulling back on investment in new projects. Barclays’ mid-year survey of oil industry executives found that spending by oil majors will be flat in 2014. Earlier the bank projected a 3% increase in spending.

In the deepwater sector, cost escalation is causing companies to slow investment decisions.

The planned $6 billion Bressay heavy oil project in the UK North Sea, for example, hit a cost wall that forced Statoil to rethink the project. Cost escalation caused Chevron to stop, at least temporarily, the $10 billion Rosebank project offshore the UK Shetlands Islands. Commenting on the cost pressures, Technip said in July that “some of our customers are taking a much slower and more combative approach.”

Compounding this, shale oil and gas development is increasingly drawing capex resources from energy companies. Rystad Energy says “spending on drilling, completion and lease equipment in North American shale plays will reach $140 billion in 2014.” The figure is up 10% from 2013 and Rystad expects similar growth in 2015.

Wood Mackenzie expects the Texas Wolfcamp tight oil play alone to draw $12 billion in capital spending in 2014. Some of the growing capital expenditures on shale projects have undoubtedly migrated from deepwater development.

The impact has been to cause some backing off on new deepwater project starts – which may explain why orders for production floaters are within, but at the low end of our forecast range.

We will examine these conflicting underlying market forces in more detail when we issue our new five year forecast of floating production system orders in September.

IMA provides market analysis and strategic planning advice in the marine and offshore sectors. Over 40 years we have performed more than 350 business consulting assignments for 170+ clients in 40+ countries. We have assisted shipbuilders, ship repair yards and manufacturers in forming a a plan to penetrate the offshore market. Our assignments have included advice on acquiring an FPSO contractor, forming an alliance to bid for large FPSO contracts, satisfying local content requirements and more.

t: 1 202 333 8501

e: [email protected]

w: www.imastudies.com(As published in the August 2014 edition of Maritime Reporter & Engineering News - http://magazines.marinelink.com/Magazines/MaritimeReporter)

-

)

March 2024 - Marine Technology Reporter page: 45

)

March 2024 - Marine Technology Reporter page: 45ronments. The new agreement will address speci? c techni- cal gaps in the UUV defense and offshore energy markets especially for long duration, multi-payload mission opera- tions where communications are often denied or restricted. As part of the new alliance, Metron’s Resilient Mission Autonomy portfolio

-

)

March 2024 - Marine Technology Reporter page: 42

)

March 2024 - Marine Technology Reporter page: 42DNV type-approved for 6km rated crewed submers- ibles. BIRNS Meridians are compact, and feature several pin con? gurations, with more in design for release later this year. The M40 pin con? guration has a single 85 square millime- ter/3-000 contact. Both standard and reverse gender versions Image courtesy

-

)

March 2024 - Marine Technology Reporter page: 37

)

March 2024 - Marine Technology Reporter page: 37plywood box potted with hot tar. A pressure-compensated pull-apart connector allowed the simple disconnect of the electrical leads as the vehicle re- leased from its ballast frame. (See Figure 4). Absorbent Glass Mat (AGM) lead-acid batteries are con- structed differently than the wet-cell battery. AGMs

-

)

March 2024 - Marine Technology Reporter page: 25

)

March 2024 - Marine Technology Reporter page: 25Auerbach explained that ideally, “one ? ed layers of geothermal activity,” noted changes over an area of 8,000 km2. They would have both instruments: seismom- Skett, “and the change in salinity and dis- found up to seven km3 of displaced ma- eters to detect and locate subsurface ac- solved particles for

-

)

April 2024 - Maritime Reporter and Engineering News page: 47

)

April 2024 - Maritime Reporter and Engineering News page: 47MARKETPLACE Products & Services www.MaritimeEquipment.com Powering the fleet for 60 years! HYDRAULIC NOISE, SHOCK AND VIBRATION SUPPRESSOR Noise, Shock, VibraO on & PulsaO on in Quiet, Smooth Flow Out Oil Bladder Nitrogen (blue) Manufactured by MER

-

)

April 2024 - Maritime Reporter and Engineering News page: 43

)

April 2024 - Maritime Reporter and Engineering News page: 43“The industry is an ecosystem which includes owners, managers, mariners, shipyards, equipment makers, designers, research institutes and class societies: all of them are crucial,” – Eero Lehtovaara, Head of Regulatory & Public Affairs, ABB Marine & Ports All images courtesy ABB Marine and Ports provi

-

)

April 2024 - Maritime Reporter and Engineering News page: 42

)

April 2024 - Maritime Reporter and Engineering News page: 42OPINION: The Final Word Seeing the Ship as a System Shipping must engage with the decarbonization realities that lie ahead by changing the way it crafts maritime legislation to re? ect its place in the interconnected, interdependent world economy, said Eero Lehtovaara, ABB Marine & Ports. ABB Marine &

-

)

April 2024 - Maritime Reporter and Engineering News page: 41

)

April 2024 - Maritime Reporter and Engineering News page: 41Nautel provides innovative, industry-leading solutions speci? cally designed for use in harsh maritime environments: • GMDSS/NAVTEX/NAVDAT coastal surveillance and transmission systems • Offshore NDB non-directional radio beacon systems for oil platform, support vessel & wind farm applications

-

)

April 2024 - Maritime Reporter and Engineering News page: 35

)

April 2024 - Maritime Reporter and Engineering News page: 35func- the phones we are estimated to un- tionality. FORCE Technology’s upcoming DEN-Mark2 math- lock around 50-80 times a day. It has ematical model release for its augmented reality SimFlex4 tug W changed us. Half the people surveyed and ship simulator will offer unprecedented model accuracy in a 2022

-

)

April 2024 - Maritime Reporter and Engineering News page: 33

)

April 2024 - Maritime Reporter and Engineering News page: 33CRANES & OFFSHORE WIND HLP is developing a crane that will enable tower HLP is developing a crane that will enable pieces to be stacked components such as towers to be stacked in multiple layers on vertically in marshalling areas. installation vessels. HLP is developing a ring crane capable of 6

-

)

April 2024 - Maritime Reporter and Engineering News page: 28

)

April 2024 - Maritime Reporter and Engineering News page: 28. It should be pointed out that we can build adaptive force packages to be placed on a number of our ships to add additional capability. MSC can also lease ship or contract Military Sealift Command’s ? eet replenishment oiler USNS Joshua Humphreys for services as needed. For example, we (T-AO 188)

-

)

April 2024 - Maritime Reporter and Engineering News page: 25

)

April 2024 - Maritime Reporter and Engineering News page: 25RADM PHILIP SOBECK, MILITARY SEALIFT COMMAND Photo by Brian Suriani USN Military Sealift Command From a global supply chain perspective, What makes MSC so vital to the we’ve learned a lot about dealing with Navy’s ? eet and our military disruptions. COVID delivered a big forces around the world? wake-up

-

)

April 2024 - Maritime Reporter and Engineering News page: 22

)

April 2024 - Maritime Reporter and Engineering News page: 22MULTIPLE US OSW WIND DEVELOPMENTS AND SEEING AN UP-TICK FOR CVA, TECHNOLOGY REVIEW AND RISK REDUCTION SERVICES IN EARLY DEVELOPMENT PHASES. WITH NEW LEASE ROUNDS COMING AND NEW OPPORTUNITIES, WE DO NOT SEE A BIG SLOWDOWN FOR OSW DEVELOPMENTS APART FROM THE OBVIOUS PROJECT DELAYS AND RE-BIDS. ROB LANGFORD

-

)

April 2024 - Maritime Reporter and Engineering News page: 16

)

April 2024 - Maritime Reporter and Engineering News page: 16MARKETS SOVs – Analyzing Current, Future Demand Drivers By Philip Lewis, Director of Research, Intelatus © Björn Wylezich/AdobeStock t a high-level, there are three solutions to transferring Lower day rate CTVs are often used for daily transfer of technicians from shore bases to offshore wind farms

-

)

April 2024 - Maritime Reporter and Engineering News page: 15

)

April 2024 - Maritime Reporter and Engineering News page: 15hydro-acoustic design of a propulsor that delays cavitation meets its underwater noise limits. This will require specialized inception and cavitating area. The third approach should be test sites or specialized mobile underwater testing equipment. isolation mounting of a vibro-active equipment and

-

)

April 2024 - Maritime Reporter and Engineering News page: 14

)

April 2024 - Maritime Reporter and Engineering News page: 14Book Review Approach to Meeting Underwater Radiated Noise Limits Def ned By Raymond Fischer uantitative underwater radiated noise limits will construction inspections, 5) possible training with respect to be developed shortly by IMO, and/or countries salient design/construction essentials, 6) compliance

-

)

April 2024 - Maritime Reporter and Engineering News page: 13

)

April 2024 - Maritime Reporter and Engineering News page: 13from gasoline to methanol, but compared to just buying an EV After some pondering, I think I can reduce it to this logi- today that is a pointless exercise. It would actually make more cal sequence: sense to buy a plug-in hybrid that is con? gured for methanol It is the carbon. We want zero carbon as

-

)

April 2024 - Maritime Reporter and Engineering News page: 12

)

April 2024 - Maritime Reporter and Engineering News page: 12Back to the Drawing Board When Efficiency Does Not Help Sustainability By Rik van Hemmen y brother and I had a discussion about methanol This study concluded that the Toyota Prius Prime is the green- where we concluded that methanol is a prom- est car you can buy in the United States. ising sustainable

-

)

April 2024 - Maritime Reporter and Engineering News page: 8

)

April 2024 - Maritime Reporter and Engineering News page: 8Training Tips for Ships © By tuastockphoto/AdobeStock Tip #58 Enhancing Behavior-Based Safety By Murray Goldberg, CEO, Marine Learning Systems ave you ever heard the term “Behaviour-Based environment where each individual feels personally respon- Safety”? Although the term itself is relatively sible for

-

)

April 2024 - Maritime Reporter and Engineering News page: 7

)

April 2024 - Maritime Reporter and Engineering News page: 7REGISTER NOW Seawork celebrates its 25th anniversary in 2024! The 25th edition of Europe’s largest commercial marine and workboat exhibition, is a proven platform to build business networks. Seawork delivers an international audience of visitors supported by our trusted partners. Seawork is the

-

)

April 2024 - Marine News page: 39

)

April 2024 - Marine News page: 39There are ? ve major paint catego- lenges in shipyards is managing small building is a multifaceted endeavor ries in new construction shipbuilding: parts, which are prone to surface rust that demands integrative systems before installation. Optimizing the planning, as well as adoption of new 1.

-

)

April 2024 - Marine News page: 33

)

April 2024 - Marine News page: 33Feature Electric Tugs ing tug design. ABB was brought on as systems integrator, and Coden, Ala. shipbuilder Master Boat Builders began building the vessel later that year. The result of these efforts is the 82-foot-long tug eWolf, built to ABS class and is compliant with U.S. Coast Guard Subchapter M

-

)

April 2024 - Marine News page: 24

)

April 2024 - Marine News page: 24from the permit) within a 42-mile- study, that vessels navigating in wind farms “could experience long offshore export cable corridor extending from the lease interference and re? ectivity due to the turbine structures and area north into Rhode Island Sound and Narragansett Bay, blades which could lead

-

)

April 2024 - Marine News page: 23

)

April 2024 - Marine News page: 23and precautionary areas, the USCG asserts, “do not intersect, limit, remove, or in any other way interfere” with further de- velopment of the Atlantic lease areas. It’s important to keep in mind, of course, that federal of? cials seek 30 gigawatts (GW) of offshore wind by 2030. Then, by 2050, 110 GW