What’s New with Floating Production?

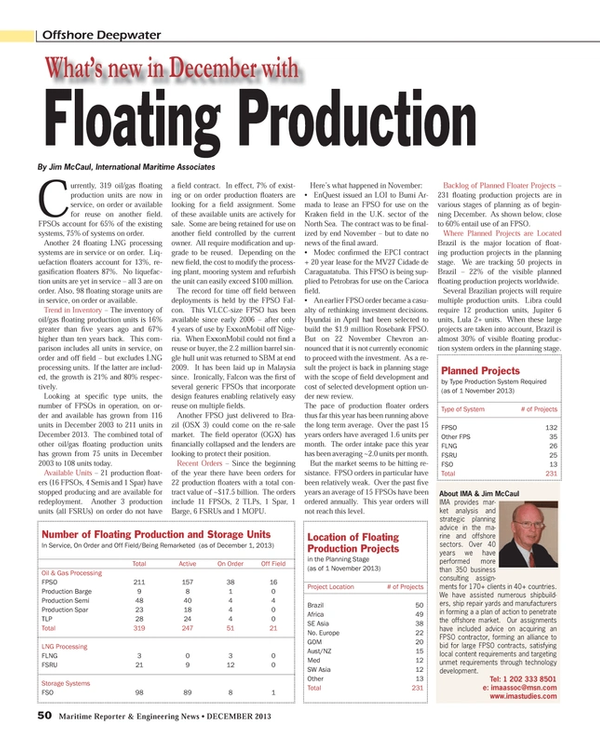

Currently, 319 oil/gas floating production units are now in service, on order or available for reuse on another field. FPSOs account for 65% of the existing systems, 75% of systems on order.

Another 24 floating LNG processing systems are in service or on order. Liquefaction floaters account for 13%, regasification floaters 87%. No liquefaction units are yet in service – all 3 are on order. Also, 98 floating storage units are in service, on order or available.

Trend in Inventory – The inventory of oil/gas floating production units is 16% greater than five years ago and 67% higher than ten years back. This comparison includes all units in service, on order and off field – but excludes LNG processing units. If the latter are included, the growth is 21% and 80% respectively.

Looking at specific type units, the number of FPSOs in operation, on order and available has grown from 116 units in December 2003 to 211 units in December 2013. The combined total of other oil/gas floating production units has grown from 75 units in December 2003 to 108 units today.

Available Units – 21 production floaters (16 FPSOs, 4 Semis and 1 Spar) have stopped producing and are available for redeployment. Another 3 production units (all FSRUs) on order do not have a field contract. In effect, 7% of existing or on order production floaters are looking for a field assignment. Some of these available units are actively for sale. Some are being retained for use on another field controlled by the current owner. All require modification and upgrade to be reused. Depending on the new field, the cost to modify the processing plant, mooring system and refurbish the unit can easily exceed $100 million.

The record for time off field between deployments is held by the FPSO Falcon. This VLCC-size FPSO has been available since early 2006 – after only 4 years of use by ExxonMobil off Nigeria. When ExxonMobil could not find a reuse or buyer, the 2.2 million barrel single hull unit was returned to SBM at end 2009. It has been laid up in Malaysia since. Ironically, Falcon was the first of several generic FPSOs that incorporate design features enabling relatively easy reuse on multiple fields.

Another FPSO just delivered to Brazil (OSX 3) could come on the re-sale market. The field operator (OGX) has financially collapsed and the lenders are looking to protect their position.

Recent Orders – Since the beginning of the year there have been orders for 22 production floaters with a total contract value of ~$17.5 billion. The orders include 11 FPSOs, 2 TLPs, 1 Spar, 1 Barge, 6 FSRUs and 1 MOPU.

Here’s what happened in November:

• EnQuest issued an LOI to Bumi Armada to lease an FPSO for use on the Kraken field in the U.K. sector of the North Sea. The contract was to be finalized by end November – but to date no news of the final award.

• Modec confirmed the EPCI contract + 20 year lease for the MV27 Cidade de Caraguatatuba. This FPSO is being supplied to Petrobras for use on the Carioca field.

• An earlier FPSO order became a casualty of rethinking investment decisions. Hyundai in April had been selected to build the $1.9 million Rosebank FPSO. But on 22 November Chevron announced that it is not currently economic to proceed with the investment. As a result the project is back in planning stage with the scope of field development and cost of selected development option under new review.

The pace of production floater orders thus far this year has been running above the long term average. Over the past 15 years orders have averaged 1.6 units per month. The order intake pace this year has been averaging ~2.0 units per month.

But the market seems to be hitting resistance. FPSO orders in particular have been relatively weak. Over the past five years an average of 15 FPSOs have been ordered annually. This year orders will not reach this level.

Backlog of Planned Floater Projects – 231 floating production projects are in various stages of planning as of beginning December. As shown below, close to 60% entail use of an FPSO.

Where Planned Projects are Located Brazil is the major location of floating production projects in the planning stage. We are tracking 50 projects in Brazil – 22% of the visible planned floating production projects worldwide.

Several Brazilian projects will require multiple production units. Libra could require 12 production units, Jupiter 6 units, Lula 2+ units. When these large projects are taken into account, Brazil is almost 30% of visible floating production system orders in the planning stage.

Location of Floating

Production Projects

in the Planning Stage

(as of 1 November 2013)

Project Location # of Projects

Brazil 50

Africa 49

SE Asia 38

No. Europe 22

GOM 20

Aust/NZ 15

Med 12

SW Asia 12

Other 13

Total 231

Planned Projects

by Type Production System Required

(as of 1 November 2013)

Type of System # of Projects

FPSO 132

Other FPS 35

FLNG 26

FSRU 25

FSO 13

Total 231

Number of Floating Production and Storage Units

In Service, On Order and Off Field/Being Remarketed (as of December 1, 2013)

Total Active On Order Off Field

Oil & Gas Processing

FPSO 211 157 38 16

Production Barge 9 8 1 0

Production Semi 48 40 4 4

Production Spar 23 18 4 0

TLP 28 24 4 0

Total 319 247 51 21

LNG Processing

FLNG 3 0 3 0

FSRU 21 9 12 0

Storage Systems

FSO 98 89 8 1

About IMA & Jim McCaul

IMA provides market analysis and strategic planning advice in the marine and offshore sectors. Over 40 years we have performed more than 350 business consulting assignments for 170+ clients in 40+ countries. We have assisted numerous shipbuilders, ship repair yards and manufacturers in forming a a plan of action to penetrate the offshore market. Our assignments have included advice on acquiring an FPSO contractor, forming an alliance to bid for large FPSO contracts, satisfying local content requirements and targeting unmet requirements through technology development.

Tel: 1 202 333 8501

e: [email protected]

www.imastudies.com

(As published in the December 2013 edition of Maritime Reporter & Engineering News - www.marinelink.com)

Read What’s New with Floating Production? in Pdf, Flash or Html5 edition of December 2013 Maritime Reporter

Other stories from December 2013 issue

Content

- Coming your way, a 3% rise in Operating Costs page: 10

- Five Minutes With: Tore Morten Olsen, Astrium Services page: 12

- Marine Cybersecurity: Is Your Ship Safe? Are You Sure? page: 16

- U.S. Export Reform: New Year, New Rules page: 18

- U.S. Port Security and the Impact of Sequester & Budget Woes page: 20

- Global Port Security and BMT Isis page: 22

- LED Lighting: Reduced Costs, Enhanced Safety page: 24

- India's Maritime Growth Fueled by Foreign Companies page: 26

- New Crane from Liebherr for Harbors, Offshore page: 28

- Ship Power: Out of the Past Comes Wärtsilä's Engine of the Future page: 30

- The Navy’s Battlewagon of the 21st Century page: 34

- Maersk’s Mammoth Containerships Making History page: 40

- New Bulk Carrier from Imabari Offers Unique Advantages page: 42

- Damen PSV 3300: A Diamond in the Rough page: 43

- Bourbon and CGG Partner for Seismic Survey Success page: 44

- Great Ships of 2013: Shuttle Tanker RIO 2016 for TEN page: 45

- Great Ships of 2013: Bow Pioneer page: 46

- Great Ships of 2013: Hornbeck’s HOSMAX 300 Series page: 47

- Great Ships of 2013: Oceanex Connaigra page: 48

- Great Ships of 2013: Hydra Voyager page: 48

- Great Ships of 2013: Damen Modular Barge page: 49

- What’s New with Floating Production? page: 50

- New Monitoring System from Rexroth page: 56

- Regal Motors Win Russian OK page: 56

- Jotun Debuts New Eco Antifouling page: 56

- New “Energy Demand Forecast System for Ships” page: 56

- Ultra Steam Turbine Plants page: 56

- Delta Plasma Rotator Launched page: 56

- LaBorde Launches New Compact Power Unit page: 56

- MTU Gensets for British Combat Ship page: 57

- Product Spotlight: Viking LifeCraft Evacuation System page: 57

- Sherwin-Williams Launch Marine Coatings App page: 57

- SMT Develops Robotic Tube Cutter page: 57

- Optimarin Inks Ballast Water Treatment Deal with V.Ships page: 57

- SturdiLED LED Floodlight Released page: 57

- IHC Debuts “Zero-Pollution” Seal page: 57